- English

- Italiano

- Español

- Français

A Trader’s Weekly Playbook: Mega Cap Earnings, Central Banks and Australian CPI

Weekly Summary

• Mega cap tech earnings in play, with 33% of NAS100 weight reporting on Wednesday

• Central bank meetings from the Fed, ECB, BOE and BOC in focus

• Australian March and Q1 CPI set to see the RBA hike on 5 May

• Geopolitics remains fluid, driving crude oil and risk sentiment

• Strong earnings and falling volatility continue to support equities

Geopolitics and crude set the tone

With Trump pulling JD Vance and his negotiating team from attending diplomatic talks in Pakistan, we initially saw buying in crude and the USD, with mild headwinds to equities. Headlines have since emerged, via Axios, that Iran has offered the US a new proposal to reopen the Strait of Hormuz. This has brought in crude sellers and provided tailwinds to risk assets.

This is one to watch closely to see if it has legs. While geopolitical headlines will continue to influence broader macro markets, the scheduled event risk for traders this week is significant.

Mega cap earnings take centre stage

It is hard to look past the deluge of mega cap tech earnings due this week, particularly those reporting after the cash close. Microsoft, Meta, Amazon and Alphabet all report, with Apple following on Thursday. This equates to over 33% of the NAS100 index weight reporting in Wednesday’s after-hours trade and around 20% of the S&P 500 index weight.

As a result, price action in US 24-hour equity CFDs and the NAS100 index could be volatile.

Tech momentum and earnings strength

There has been significant focus on the NAS100, and flows have increased accordingly. The market is fully engaged in the tech trade, particularly in AI leaders, infrastructure and power generation, as well as hardware, memory and compute plays.

So far, 27% of the S&P 500 have reported earnings, with strong results. Around 78% have beaten expectations by an average of 10%. Consensus EPS growth for the quarter is now tracking just under 16%, with full-year expectations at 18.6%.

Intel delivered strong numbers last week, supporting sentiment, while TSMC results have provided a positive read-through to Nvidia, now trading at $208 with a market cap of $5.08 trillion.

Lower realised volatility has also supported equities. The 20-day realised volatility in the S&P 500 has declined from 20% in early April to 14%. It pays to be long equities when volatility is falling, as the ensuing passive flows that come from lower volatility promote a new leg higher in equity.

The market had entered April neutral to underweight tech, pricing in concerns around AI disruption, private credit risks to banks, Brent crude rising to $150, and potential Fed hikes. There were also expectations of escalation in the US-Iran conflict.

These views have not materialised, and investors have rotated back into tech in size. Positive developments around AI demand and usage, including updates from Anthropic, have helped. Investors are also increasingly comfortable with capex plans and expected returns. Meta remains a key risk given past headwinds from heavy investment cycles.

Central banks in focus, but no fireworks expected

Central bank meetings are plentiful this week, with the Fed, ECB, BOE and BOC all in focus. None are expected to change policy, and the Fed in particular is likely to remain patient. Geopolitics remains uncertain, with crude rebounding last week. While a ceasefire remains possible and talks may occur remotely, the Strait of Hormuz is still blocked. The longer this persists, the greater the potential impact on inflation and demand. For now, corporate earnings remain resilient and US companies continue to manage conditions well.

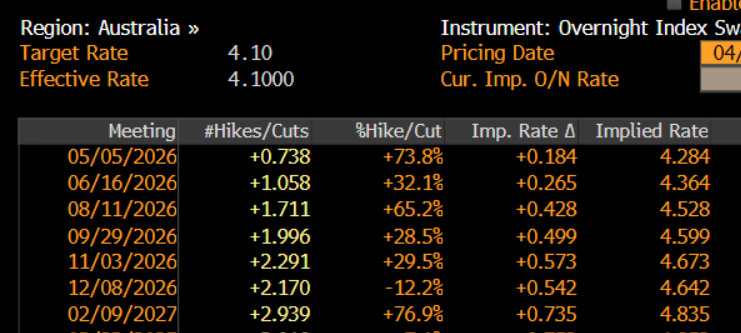

Australian CPI and RBA expectations

In Australia, the key event is the March and Q1 CPI report on Wednesday. Monthly headline inflation for March is expected at 4.8% y/y, with core inflation at 3.3% y/y, reflecting the impact of higher energy prices.

Q1 core CPI is expected to rise 0.9% q/q, taking the annualised rate to 3.5%. A stronger outcome, closer to 1% q/q, would likely result in a 25 basis point RBA rate hike in May.

Markets currently imply a 74% probability of a hike on 5 May. Another 25 basis point increase would take the cash rate to 4.35%, effectively reversing all easing implemented post Covid.

ASX200, banks and AUD outlook

The ASX200 has lagged global equity markets, with the major banks falling out of favour with investors. Upcoming earnings from ANZ, WBC and NAB, alongside the RBA meeting, will bring additional focus to the sector. The AUD remains in consolidation against the USD and major crosses. There is little evidence of a strong trend, with price action largely range-bound and two-way for now.

Good luck to all.

The material provided here has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such is considered to be a marketing communication. Whilst it is not subject to any prohibition on dealing ahead of the dissemination of investment research we will not seek to take any advantage before providing it to our clients.

Pepperstone doesn’t represent that the material provided here is accurate, current or complete, and therefore shouldn’t be relied upon as such. The information, whether from a third party or not, isn’t to be considered as a recommendation; or an offer to buy or sell; or the solicitation of an offer to buy or sell any security, financial product or instrument; or to participate in any particular trading strategy. It does not take into account readers’ financial situation or investment objectives. We advise any readers of this content to seek their own advice. Without the approval of Pepperstone, reproduction or redistribution of this information isn’t permitted.