- English

- Italiano

- Español

- Français

March 2025 US Employment Report: None Of This Really Matters Now

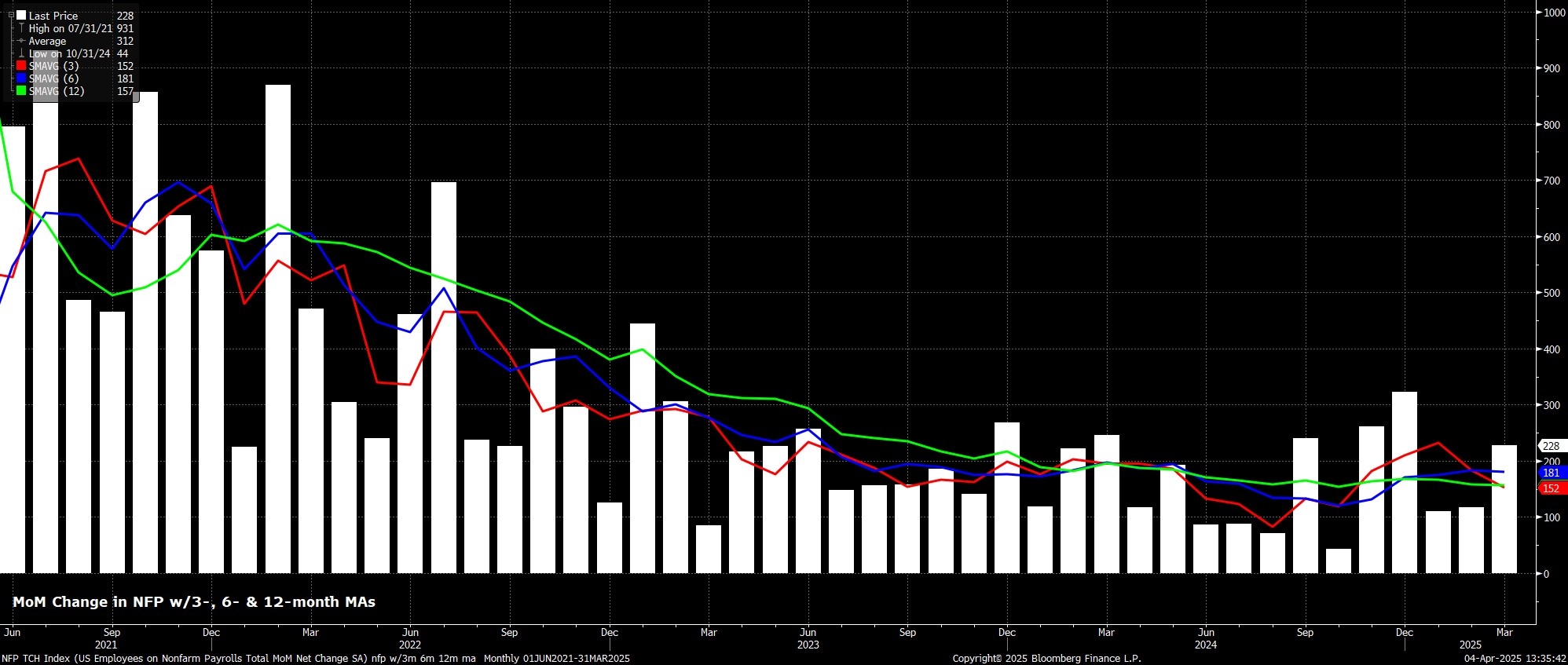

Headline nonfarm payrolls rose by 228k last month, above consensus expectations for a +140k increase, and above the typically wide forecast range of +80k to +200k. Simultaneously, the prior two payrolls prints were revised by a net -48k, in turn taking the 3-month average of job gains to +152k, its lowest level this year.

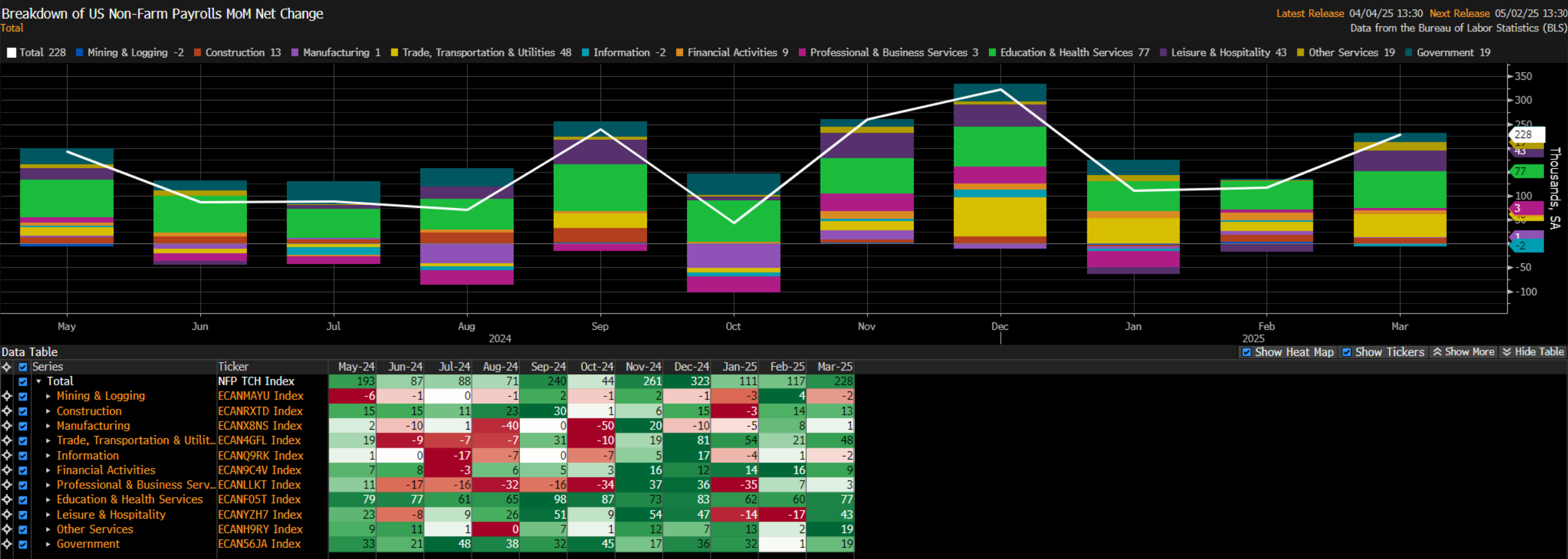

Digging a little deeper into the data, the sectoral split pointed to broad-based job gains, with only Mining & Logging and Information shedding jobs, marginally, on the month. The biggest gain came from Education & Health Services, while the return of striking retail workers added around 24k to the headline print.

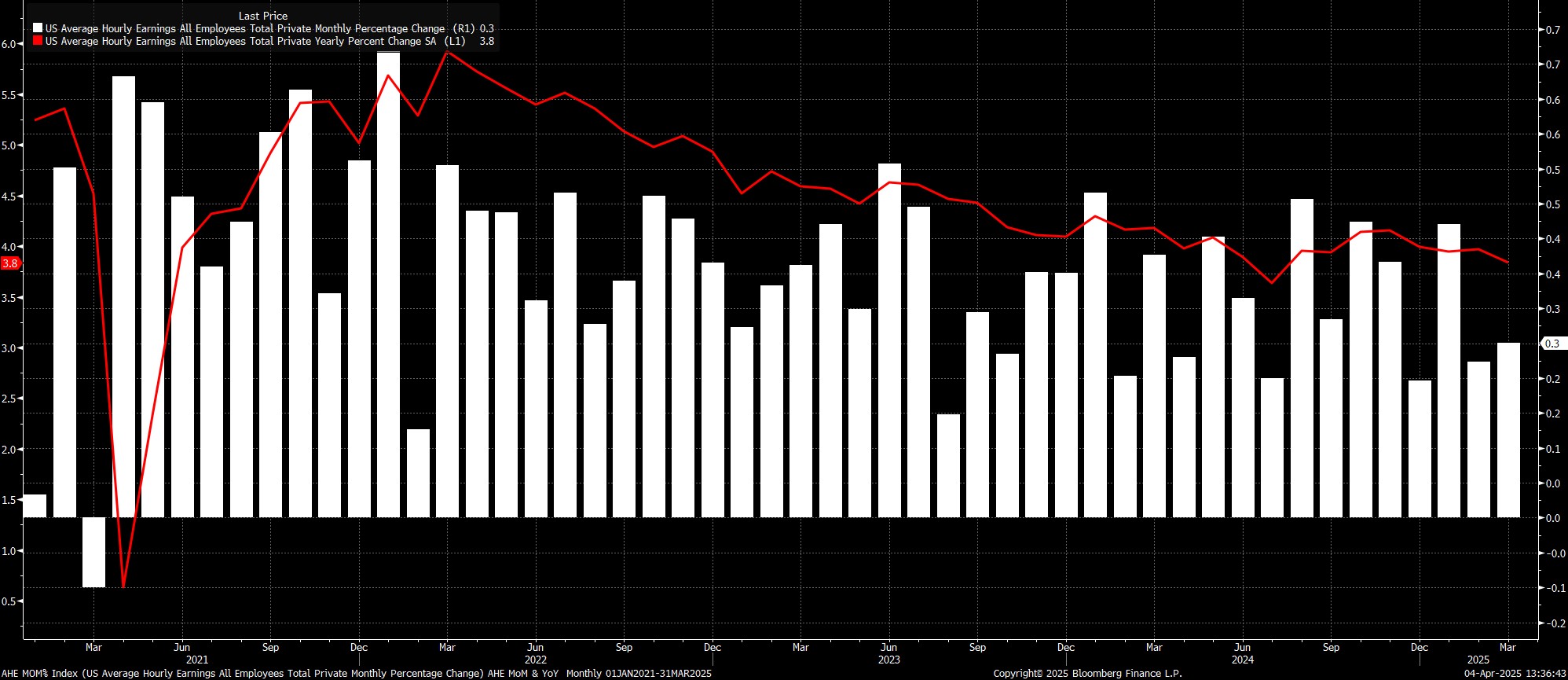

Sticking with the establishment survey, the jobs report pointed to earnings pressures remaining relatively contained. Average hourly earnings rose 0.3% MoM, in line with the pace seen last time out, which in turn saw the annual rate dip marginally to 3.8% YoY.

As has now been the case for some time, data of this ilk reinforces the FOMC’s long-standing view that, at present, the labour market is not a notable source of inflationary pressures; though, of course, this week’s reciprocal tariff announcement represents significant upside risk on that front anyway.

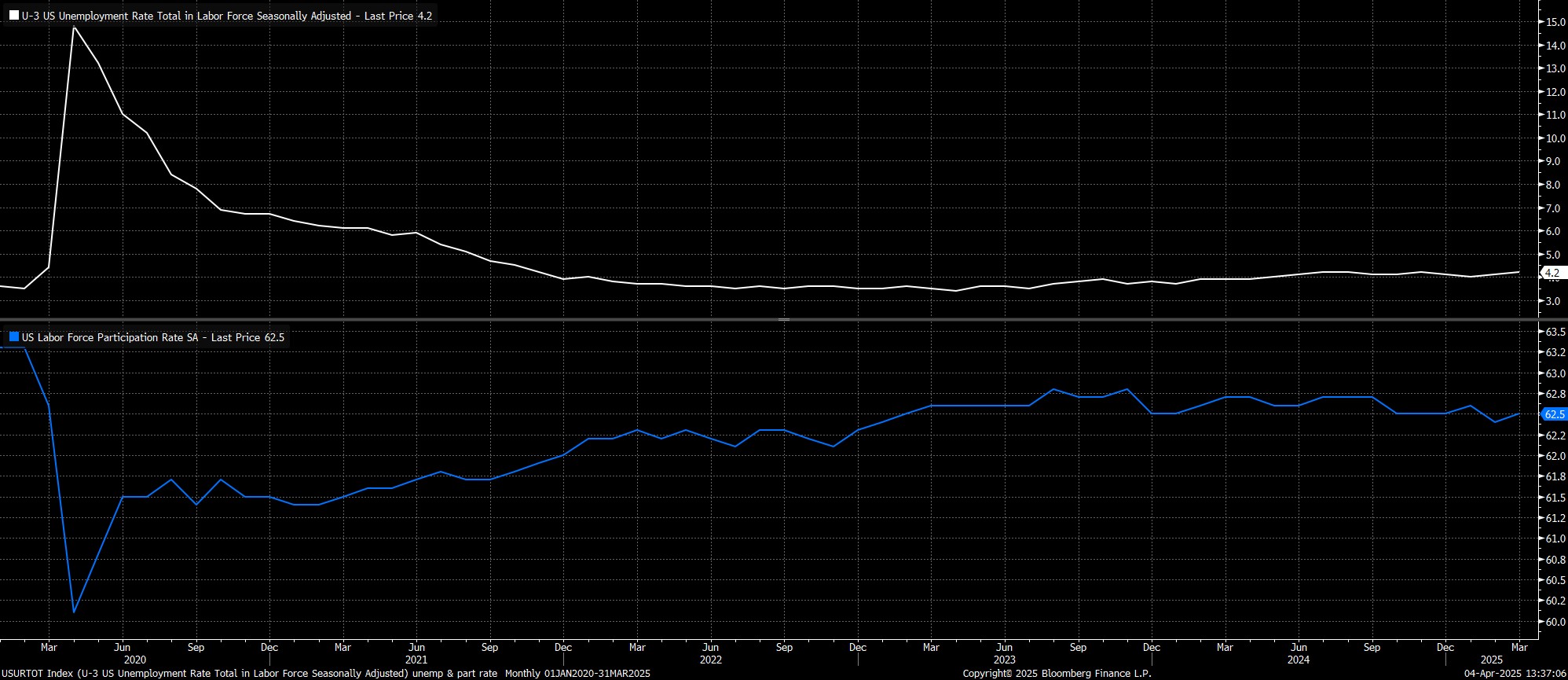

Turning to the household survey, unemployment ticked higher to 4.2% in March, likely a function of higher labour force participation, with the participation rate rising to 62.5%, paring half the decline seen in Feb.

Of course, a health warning must continue to accompany the HH figures, with the BLS continuing to struggle with falling survey response rates, and accounting for the changing composition of the labour force due to the impacts of immigration. Hence, the survey has proved extremely volatile, and a little unreliable, for the bulk of this cycle.

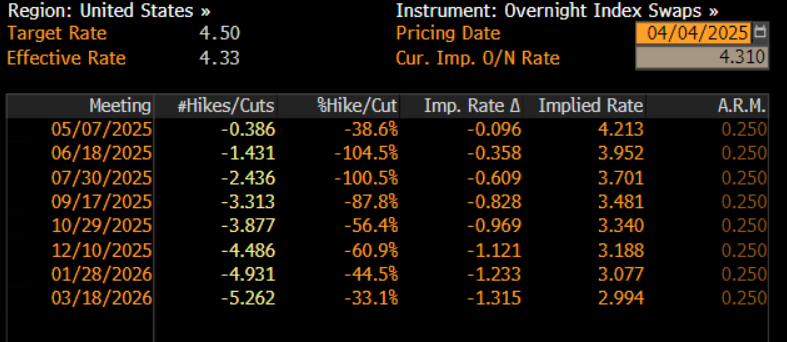

As the jobs report was digested, money markets barely budged, though continue to price an uber-dovish Fed outlook, amid downside growth risks induced by tariffs. As such, participants still see around a 45% chance of a 25bp cut in May, fully price the next 25bp cut for June, and price 110bp of easing by year-end.

Taking a step back, I’m left asking myself the question – does any of this data actually matter?

The obvious answer to that question is ‘no’. Obviously, the jobs report is backward-looking, and frankly ‘old news’ by this point, referencing the employment situation as it was three weeks ago. Since then, the US economy has undergone a huge paradigm shift, not only as uncertainty continues to cloud the outlook, but also as President Trump’s ‘reciprocal’ tariffs go into effect, more than doubling the average effective tariff rate to its highest level in a century.

Clearly, it is too early for the impacts of this uber-protectionist trade policy to become known, though the upside inflation, and downside growth, risks that the tariffs pose are both clear, and sizeable in nature.

This leaves FOMC policymakers in something of a bind, needing to mull whether a more rapid pace of policy normalisation to support growth, or a slower pace of normalisation amid more intense price pressures, is the appropriate course of action.

For the time being, Powell & Co are likely to remain on the sidelines, methodically examining and modelling tariff announcements as they are made, and closely watching incoming economic data.

That said, assuming the announced tariffs remain in place, the bar for rate cuts at any stage over the next couple of quarters is now an incredibly high one, with tariff-induced inflation trumping the meaningful downwards pressure that those tariffs will exert on economic growth, in terms of potential monetary policy responses. My base case is that the FOMC will be unable to look-through the near-term inflationary impulse from tariffs, likely waiting to see actual evidence of this impulse being temporary, before being comfortable to take further steps back towards a more neutral fed funds rate.

The material provided here has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such is considered to be a marketing communication. Whilst it is not subject to any prohibition on dealing ahead of the dissemination of investment research we will not seek to take any advantage before providing it to our clients.

Pepperstone doesn’t represent that the material provided here is accurate, current or complete, and therefore shouldn’t be relied upon as such. The information, whether from a third party or not, isn’t to be considered as a recommendation; or an offer to buy or sell; or the solicitation of an offer to buy or sell any security, financial product or instrument; or to participate in any particular trading strategy. It does not take into account readers’ financial situation or investment objectives. We advise any readers of this content to seek their own advice. Without the approval of Pepperstone, reproduction or redistribution of this information isn’t permitted.