CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 72.2% of retail investor accounts lose money when trading CFDs with this provider. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

- English

- Italiano

- Español

- Français

The Fed and the ECB are almost done tightening, and market pricing (in swap markets) shows this front and centre. In the case of the US, core PCE inflation and the Employment Cost Index (ECI) showed that price pressures and wages are abating. The US Q2 GDP print grew at an above-trend pace (at 2.4%) - risky assets find inspiration at a resilient economy at a time when the Fed is close to completing its cycle and inflation grinds lower.

Add in a 4.5% rally in Chinese equity on the week, and the word ‘Goldilocks’ and ‘immaculate disinflation’ comes up liberally in conversation. It’s no wonder the chase for performance is on, and those underweight equity are feeling the heat.

The positive growth factor seen in the US economy is certainly not true of Europe and China, where growth has been consistently missing the mark – the US exceptionalism story is therefore firmly in play and keeps me constructive on the USD, even if the technicals/price action are not showing any strong bias to own USDs over other G10 FX.

We see that the bullish trend in DM equity markets is mature and, in some cases, owned/loved – however, new highs seem more likely than not - Apple will need to impress in earnings this week. In Asia, it feels hard to trust the late-week rally in the HK50 or CHINAH, but I’m skewed long for another 3-5% upside. Huge inflows into mainland Chinese equities last week suggest more is to come.

The BoJ threw a curve ball into the market on Friday with its cosmetic change to YCC – in essence, it was a brilliant move by the central bank, and they’ve managed to bridge the volatility that would come with a straight change to a -/+ 1% range in the YCC band – they’ve given themselves all the flexibility should they wish to tighten policy in the future without tidal waves in global bond markets.

After the fourth biggest trading range of 2023 on Friday in USDJPY, we should see the daily ranges settle in the days ahead – Again, I don’t trust the last session sell-off in the JPY, notably vs the ZAR, MXN, and GBP, and we watch to see if the JP 10yr JGB grinds towards 75bp and above.

We look forward to another big week of event risk – the BoE should hike by 25bp, while the RBA meeting is perhaps underpriced but line ball, and we know once we get the policy call, the AUDUSD should revert to following USDCNH. US NFP should again highlight that the US labour market is in fine health, and EU inflation should offer a view that the ECB can’t be complacent but are close to the end.

It's another week in paradise and managing risk and achieving correct position sizing will help you stay solvent.

The marquee event risks for the week ahead:

US Q2 earnings – while the bulk of the S&P500 market cap has reported Q2 earnings, in the week ahead, we get a further 15% of the market cap reporting. Numbers from the Apple and Amazon (both on 3 August) and QUALCOMM get the attention. Can we continue to grind towards new highs in the US500 and NAS100?

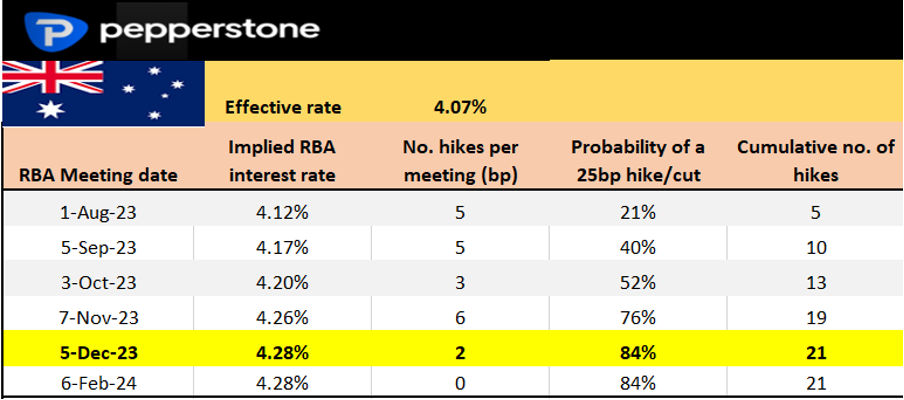

RBA meeting (1 Aug at 14:30) – Given the recent domestic economic data flow, it will be a close call whether the RBA leave the cash rate at 4.1% or hike by 25bp. Interest rate futures price a 21% chance that the RBA leave rates on hold. I personally lean to a hold from the RBA – however, given the strength in the labour market data, increasing unit labour costs and house price data, one could argue this is under-pricing the risk of a hike.

Aussie interest rate futures pricing:

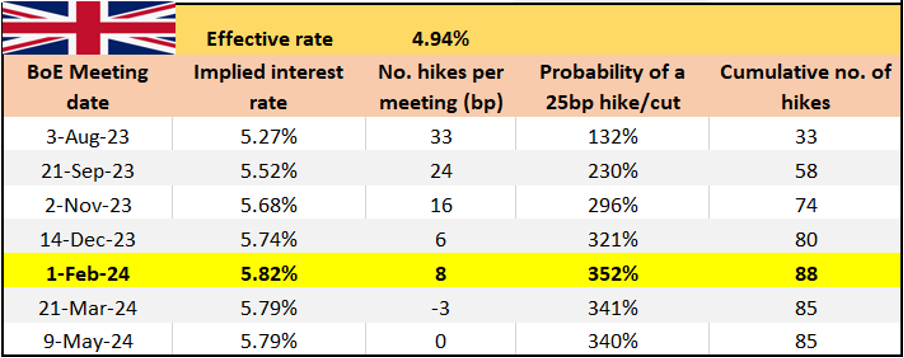

Bank of England (BoE) meeting (3 August at 21:00 AEST) - the BoE will choose between another pro-active 50bp hike or a more data-reactive 25bp hike. The market and economists see a higher probability of a 25bp hike, with the peak Bank rate expected to hit 5.83% by February 2024. We may also hear of an increased pace of quantitative tightening (QT) from October, although the BoE may wait until the September BoE meeting to update the market on this.

UK swaps pricing

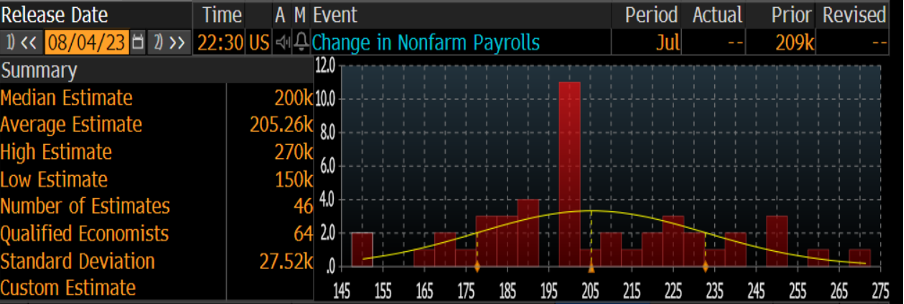

US nonfarm payrolls (NFP - 4 August at 22:30 AEST) – the US labour market remains in rude health, and there are no clear signs of a cooling in the July employment data. In the lead-up to NFP, we get ADP private payrolls and the JOLTS job openings report, so both could shape expectations for NFP.

The consensus for NFP from economists is for 200,000 jobs to have been created, with the unemployment rate expected at 3.6%. Average Hourly Earnings (AHE) will be closely watched, as wages are a key consideration if the Fed are to go on an extended pause. The consensus is we see AHE +0.3% MoM / 4.2% YoY (from 4.4%).

US ISM manufacturing (2 Aug 00:00 AEST) – The market looks for the index to come in at 46.9 (from 46.0), so a slight improvement from the June print. The ISM services print (due on 4 August) is also due this week and may be more influential on the USD. The market expects a slower pace of growth in the service sector, with the index expected to print 53.0 (from 53.9 in June). A read below 50 in services ISM would likely see broad-market volatility pick up.

Fed Senior Loan Officer Opinion Survey (1 Aug 04:00 AEST) – the SLOOS report on bank lending standards was referred to on several occasions at last week’s FOMC meeting – we expect a slowdown in credit and tighter lending, but whether this proves to be a volatility risk for markets is a key factor. Watch the US banks closely - the XLF and KBE ETFs offer good context here.

China Manufacturing and Services PMI (31 July 11:30 AEST) – after last week’s Politburo meeting, there may be a limited reaction to this PMI report, as stimulus takes time to feed through to the real economy. For now, the market looks for the manufacturing index to come in at 48.9 (from 49.0) and services PMI at 53.0 (53.2) – a read below 50 shows contraction from the prior month, and above 50 signals expansion.

EU CPI inflation (31 July 19:00 AEST) – the market expects the EU CPI estimate to come in at 5.3% (from 5.5%), with core CPI eyed at 5.4% (from 5.5%). The market currently prices 10bp of hikes for the next ECB meeting on 14 September; a 40% chance of a hike. An inflation print below 5.1% would be a surprise and should attract decent EUR sellers. Above 5.6%, and pricing for a September hike will increase, and the EUR should find a stronger tone.

EU manufacturing and services PMI (3 August 18:00 AEST) – this data point is a revision of the numbers announced on 24 July, so unless we get a marked revision to the preliminary print, the data shouldn’t move the dial too intently. The market will be watching revisions to the service data more closely.

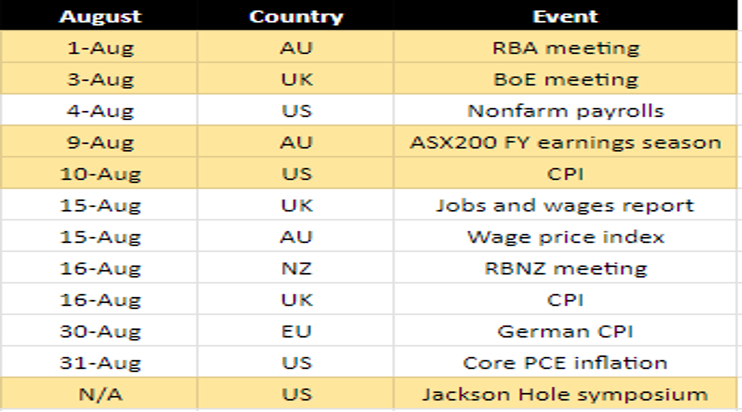

Key event risks traders need to navigate through August:

Related articles

_(3).jpg?height=420)

_(1).jpg?height=420)

The material provided here has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such is considered to be a marketing communication. Whilst it is not subject to any prohibition on dealing ahead of the dissemination of investment research we will not seek to take any advantage before providing it to our clients.

Pepperstone doesn’t represent that the material provided here is accurate, current or complete, and therefore shouldn’t be relied upon as such. The information, whether from a third party or not, isn’t to be considered as a recommendation; or an offer to buy or sell; or the solicitation of an offer to buy or sell any security, financial product or instrument; or to participate in any particular trading strategy. It does not take into account readers’ financial situation or investment objectives. We advise any readers of this content to seek their own advice. Without the approval of Pepperstone, reproduction or redistribution of this information isn’t permitted.