- English

- 中文版

In effect, being long commodity CFDs especially industrial metals (like Copper) and or short the JPY are one simultaneous short volatility position. Conversely, if long the JPY the play is for higher volatility and risk aversion.

Both historically can be good indicators or red flags in other markets, such as equities and indices CFDs.

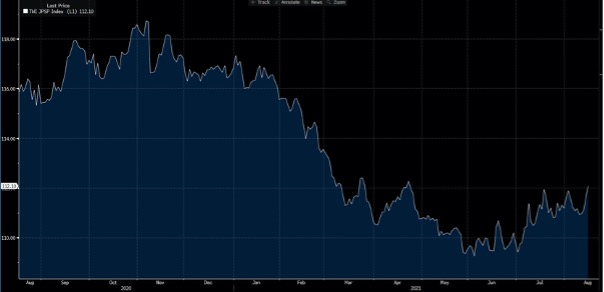

Trade-weighted JPY

(Source: Bloomberg)

One interesting dynamic is that despite the S&P 500 pushing all-time highs and implied volatility (VIX index) near 52-week lows, the trade-weighted JPY is the highest since April and rising. In fact, over the past one month the JPY and the CHF are the strongest major currencies. This seems an interesting divergence and perhaps the JPY is telling us a message of future equity volatility?

Copper was looking strong in late July, but the structure has changed and there is an air of vulnerability about it – a breakthrough 423 and then 416 and the 200-day MA at 400 may come into play. The AUD is naturally a play on commodity CFDs but also has its own domestic worries with perineal lockdowns in NSW and Victoria, but it's no surprise to see the trade-weighted AUD the weakest since December.

AUDJPY must be on the radar with price now at the range lows and eyeing a break of the 80.00 – if the figure goes this could move markedly lower. Some would have noticed the looming death cross (the 50-day crosses below the 200-day MA), although my backtesting suggests this offers little edge to traders.

AUDJPY daily

(Source: Tradingview)

There's an air of unease in global markets, but the broad market volatility isn’t there, yet. Everyone is on standby for it to happen – but timing is everything and when it comes it may not last long.

An economic slowdown impacting sentiment

We’ve seen some concerns on an economic front, with a woeful University of Michigan consumer confidence print – to understand how bad it was read this musing from the Chief Economist.

The more highly watched Conference Board consumer confidence print on 1 September could be market moving, as will the US payrolls print two days later. US small business confidence is losing momentum, while global manufacturing has grown at a slower pace for two consecutive months. China is slowing down – its credit impulse is headed lower, while the resurgence of COVID has clearly impacted and measures to control pollution ahead of the Winter Olympics could have a big impact on import demand for raw materials.

It's not all doom and gloom though – the global corporate sector is seeing margin expansion and superb earnings growth. The US service sector is working well, and the labour market should be expected to see further improvement.

Still, there is a slowdown underway, the US 30-year Treasury and real rates are telling us this and falling global liquidity is becoming less of a supportive factor. There is a 65% chance of a rate hike (from the Fed) priced by the end-2022. The idea then of central banks normalising policy in an environment of flatter yield curves, a slower rate of change in Chinese, US and global growth amid sticky inflation seems a somewhat toxic combination for markets and one where a policy mistake rises. Being long the JPY makes for a good hedge in this dynamic.

Equity markets are holding at all-time highs, but all is not so rosy under the hood - funds are rotating out of cyclical sectors (such as banks and energy) and into quality (strong balance sheets, high return on equity) and defensives (such as staples and utilities). Until funds give up on defensives and credit spreads widen then equity will hold up – a return to work post-Northern Hemisphere Summer may see the big hitters bring some much-needed volume back to markets and maybe volatility will kick up.

In the meantime, the JPY goes about its business and may get a further boost if commodity CFD really roll over – global data trends, and further tapering discussions will dictate that. The fact that Japan runs a 3.3% current account surplus makes the JPY incredibly attractive in times of risk aversion as speculators front run the idea of Japanese money managers and corporations increasing hedging ratios and repatriating capital to domestic markets.

(Source: Tradingview)

Positioning is a factor with both leveraged funds and asset managers are running a sizeable short JPY position. Adding to positioning, sentiment in the JPY is as worse than any other major currency and that is supportive.

Put the JPY and our commodity CFD markets on the radar – we may not be seeing great volatility in equities, but the rotation masks some interesting trends. Economic data is largely ok, but there are a few red flags, and normalising policy in that dynamic may not sit well with the market. The JPY may tell us all we need to know – it may well already be doing so. Trade the opportunity with Pepperstone.

Related articles

Ready to trade?

It's quick and easy to get started. Apply in minutes with our simple application process.

The material provided here has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such is considered to be a marketing communication. Whilst it is not subject to any prohibition on dealing ahead of the dissemination of investment research we will not seek to take any advantage before providing it to our clients.

Pepperstone doesn’t represent that the material provided here is accurate, current or complete, and therefore shouldn’t be relied upon as such. The information, whether from a third party or not, isn’t to be considered as a recommendation; or an offer to buy or sell; or the solicitation of an offer to buy or sell any security, financial product or instrument; or to participate in any particular trading strategy. It does not take into account readers’ financial situation or investment objectives. We advise any readers of this content to seek their own advice. Without the approval of Pepperstone, reproduction or redistribution of this information isn’t permitted.