- English

- 中文版

An announcement will be made at 17:30 EDT, conveniently just before the futures open. Vaccine’s aside, politics will continue to dominate with the RNC, while Jay Powell’s Jackson Hole speech gets the dominant share of attention in a quiet week for data. I question how much is already baked in, and how much he will unveil ahead of the 18 September FOMC meeting.

I lay out the known event risks I'm watching and some trading thoughts about these below, in the week ahead. I've also looked at this notion of poor market breadth, which is arguably the big talking point on the floors and on social media. When will it end and what will it take to reverse the crazy moves in Tesla, Apple and Amazon, if at all?

What’s in focus in the week ahead

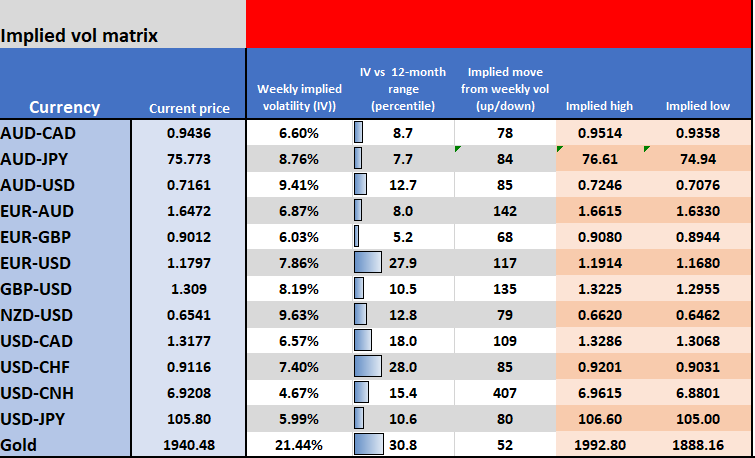

Weekly (options) implied volatility matrix, with implied moves and ranges

Monday

US – The Republican National Conference starts in Charlotte, NC. Trump is due to deliver a speech titled “Land of Greatness” on Thursday. The RNC is unlikely to be a volatility event, but there is little doubt the election is getting ever greater attention from clients and the market, where implied volatility around the 4 November election is certainly elevated relative to say the 2016 election.

Tuesday

Germany – August IFO survey (18:00 AEST) – this is broken into three sub-components – business climate (consensus expects 92.2 from 90.5 in July), expectations (98.0 from 97.0) and current assessment (86.6 from 84.5). It is worth watching GER30 exposures into this announcement, with the index printing a series of lower highs and low, and looking vulnerable for a potential re-test of the 200-day MA should sentiment sour. Lots of focus on the record EUR future long position held by non-commercial accounts (CFTC report), which may be one reason EURUSD is finding supply easy to come by above 1.1900.

Wednesday

NZ – July trade balance (08:45 AEST) – A surplus of NZD285m is expected, with exports expected to print NZ$4.91b and imports NZD4.63b. Unlikely to be a vol event for the NZD, with traders seeing greater indecision, as portrayed by the doji on the NZDUSD weekly – hard to call this pair, but the preference is to trade this from the short side.

Australia – Q2 construction work done (11:30 AEST) – Consensus is for a 7% decline. Unlikely to be a volatility event for the AUD.

US – August consumer confidence - the market expects this to tick up to 93.0 from 92.6. Has held a strong correlation with the S&P500 over the years, so it would not surprise to see this data point higher.

Thursday

UK – BoE Chief Economist Andy Haldane speaks at Edinburgh (02:00 AEST). Could be interesting for GBP traders, although GBPUSD 1-week implied volatility sits at the 10th percentile of the 12-month high-low range and therefore traders are not expecting fireworks here. Cable bulls will want a close above 1.3250 for 1.35 to come into play.

Australia – Q2 Private capital expenditure (11:30 AEST) – the market expects an 8.2% decline (economist range is -15% to -5%) in Q2, with spending unsurprisingly shelved due to COVID19. This would represent the second-largest decline ever in the series and will be a key component of the Aussie Q2 GDP calculation released on 2 September. The third estimate of corporate spending intentions for FY21 will also be released with expectations of around $80b. Hard to do much with AUDUSD given so much will hinge on Jay Powell’s speech at Jackson Hole – prefer AUDJPY or AUDCAD shorts, or EURAUD longs, but only on a closing break of 1.6557. Eyes on AUDNZD given the sizeable gravestone doji on the weekly chart – if this kicks lower then it could confirm the bull move from 1.0650 has come to an end.

Canada – Q2 current account balance (22:30 AEST) – the market expects this to push out to $12.1b. Unlikely to be a vol even for the CAD, with traders gearing up for the BoC gov’s speech at 01:15 AEST at Jackson Hole.

US – Weekly jobless and continuing claims (22:30 AEST) – the trend of improving labour statistics should be seen, with the market expecting new claims at 1m, while continuing claims should come in at 14.4m.

US – Fed chair Jay Powell speaks at the Jackson Hole Symposium at 23:10 AEST. Easily the marquee event of the week, with his speech revealing the findings of the Fed’s long-running review on monetary policy. There is little doubt Powell will be dovish, but how much is priced in is the question we should ask, and traders will be keen to see how close they are to moving to a more defined forward guidance, and specifically the appetite to move sooner to average inflation targeting. After some disappointment from the July minutes, this is the stage for the market to learn more about where the Fed really sit with potential policy changes.

The bond market is key here, and if Jay Powell can guide inflation expectations higher here, while keeping nominal yields anchored, then the USD bear trend will continue, while gold and tech fire up. Conversely, if the market is disappointed then the real yield could move higher, compelling USD shorts to cover, gold will be hit and the idea of poor breadth/participation in equity markets could actually matter.

Friday

Canada – Bank of Canada Gov Tiff Macklem speaks at Jackson Hole (due at 01:15 AEST) although the topic of the speech has not yet been disclosed. USDCAD trades in a bear channel and subsequently if trading that, then rallies into 1.3280 could be sold.

Canada – June GDP (22:30 AEST) – the market is expecting a 5.6% gain in June (month-on-month), with the year-on-year print coming in at -8.9%. We can also see expectations for the quarterly annualised print due at -39%. Again, not expecting this to move the dial too intently.

UK – BoE Gov Bailey speaks at Jackson Hole Symposium (23:05 AEST), GBP exposures warrant due consideration here.

US – we see July personal income and spending at 22:30 AEST, with consensus at -0.4% and 1.5% respectively. At the same time, we get core PCE deflator (YoY consensus at 1.2%). The University of Michigan release its sentiment survey at 00:00 AEST, with expectations for an unchanged read at 72.8.

Tesla – Last chance saloon for traders to buy Tesla before the 5 for 1 share split before price goes ex. Of course, this means little for holders other than the share price is lower and it could encourage more retail involvement. However, with the share price having rallied 50% since announcing the split, could this be set-up for a buy the rumour, sell on fact? The poster child of speculation is in beast mode and one suspects traders will be lining up to buy pullbacks in this name, that is until the fundamental backdrop discourages growth share CFDs and a sustained rotation into value.

Apple – Apple announced a 4 for 1 share split on 30 July, its fifth split since listing. Again, if you’re holding 1% of the company, you’ll still be holding 1% of the company post-split, but some see a lower price synonymous with increasing participation given the lower price. Always keen to watch Apple as it's the dominant force in markets, but there is such unwavering love for this name that it scares.

Related articles

Ready to trade?

It's quick and easy to get started. Apply in minutes with our simple application process.

The material provided here has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such is considered to be a marketing communication. Whilst it is not subject to any prohibition on dealing ahead of the dissemination of investment research we will not seek to take any advantage before providing it to our clients.

Pepperstone doesn’t represent that the material provided here is accurate, current or complete, and therefore shouldn’t be relied upon as such. The information, whether from a third party or not, isn’t to be considered as a recommendation; or an offer to buy or sell; or the solicitation of an offer to buy or sell any security, financial product or instrument; or to participate in any particular trading strategy. It does not take into account readers’ financial situation or investment objectives. We advise any readers of this content to seek their own advice. Without the approval of Pepperstone, reproduction or redistribution of this information isn’t permitted.