- English

- 中文版

We saw some excitement in the AUD after RBA governor Lowe spoke in early London trade, with AUDUSD pushing into 0.6795 and forging a 27-pips range in a five minute period – that doesn’t sound too dramatic, but consider the sheer lack of volatility and it felt like a mini-GFC!

With the market exploring the catalyst for future RBA bond purchases (known as quantitative easing or ‘QE’), and several investment banks pencilling RBA bond purchases into their 2H20 forecasts, we heard a very timely speech on “Unconventional Monetary Policy” from RBA Governor Lowe. The key take-out was the line that “our current thinking is that QE becomes an option to be considered at a cash rate of 0.25 per cent, but not before that. My fifth, and final, point is that the threshold for undertaking QE in Australia has not been reached, and I don't expect it to be reached in the near future”.

Dr Lowe also went on to explore, “it is difficult to be precise, but QE would be considered if there were an accumulation of evidence that, over the medium term, we were unlikely to achieve our objectives. In particular, if we were moving away from, rather than towards, our goals for both full employment and inflation, the purchase of government securities would be on the agenda of the Board. In this world, I would hope other public policy options were also on the country's agenda”.

Why is this speech important?

This is an important speech as strategists have been building their policy framework, not just around the probability, but the subsequent triggers for QE to eventually be enacted. There s also increasing debate as to how the AUD trades into any future announcement of RBA asset purchases, and then in the months after. One also questions dynamics in the housing market given the RBA will be buyers of RMBS (Residential Mortgage Backed Securities) and there may well have to be an offset from the regulator APRA.

QE would be a big deal for Australia, and would resonate strongly in all parts of Aussie markets, and while the size of the program would determine the extent of balance sheet expansion, we have to think it will cause a sizeable move lower in the AUD – and almost certainly well before it was formally announced.

The interesting aspect from Lowe’s comments is that the barrier to such a program is both incredibly high and unlikely until after a further 50bp cut to the cash rate, and a material tightening of financial conditions and inflation expectations. Never say never, as the fact is, if we are going to see unconventional monetary policy it will be QE and certainly not negative interest rates and while their appetite for QE is low, the bank is communicating its scenario planning to the market. Recall, this is a bank who don’t have a brilliant forecasting record 12 months out.

Also, just like we saw from Fed chairs Greenspan, Bernanke, Yellen and now Powell, there is an equity put evolving in the Aussie equity market. That being said, if economics and notably, inflation expectations really start to crumble then the market will position for future QE. That's where the ‘easy money’ is to be made.

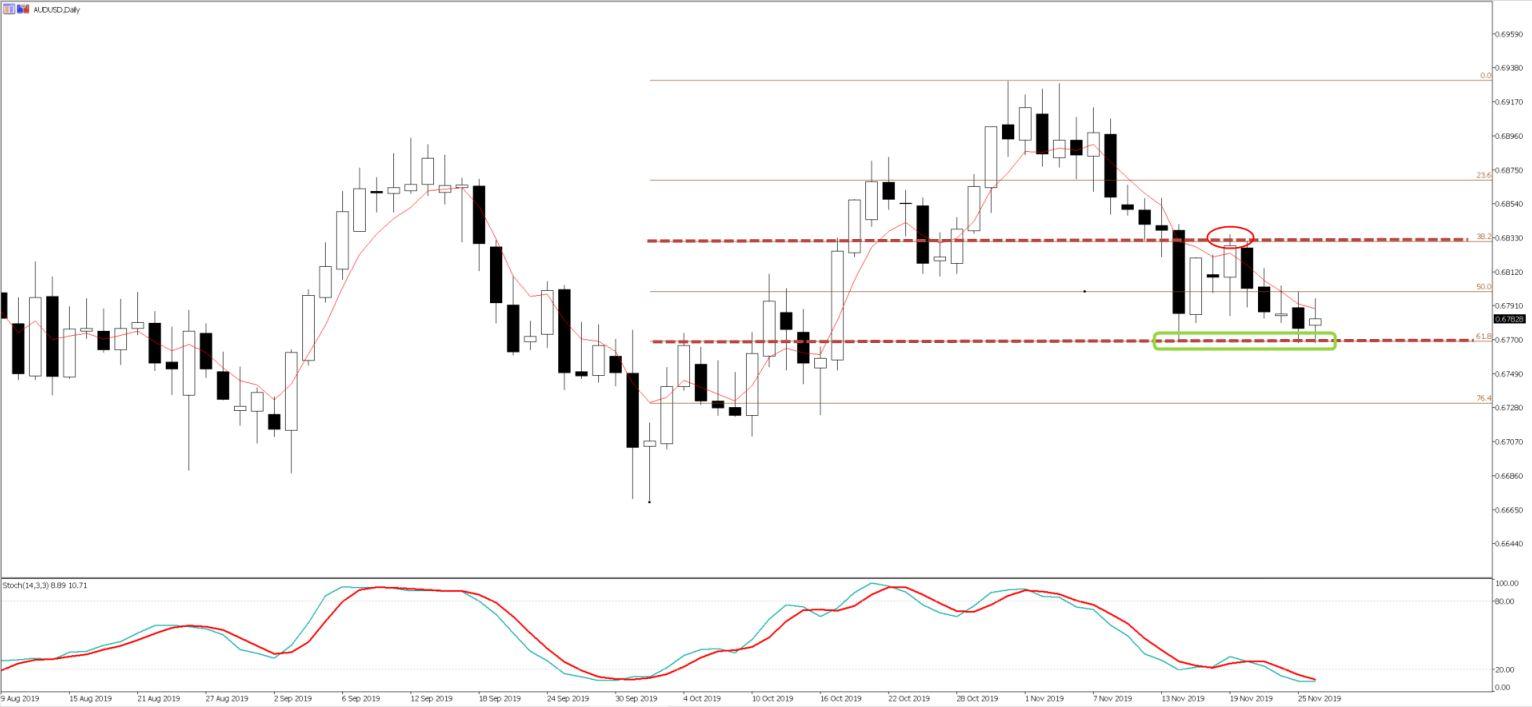

The AUDUSD failed to fizzle on Lowe’s comments, but looking at the feel of the pair price is confined to a 0.6770 to 0.6830 range, which is defined on the daily. The 5-day EMA is containing the bear trend and rallies are sold into this short-term average, where my own preference is to wait for a closing break of 0.6770 before entering shorts, as that would be incredibly significant.

QE is not a market factor yet, as we know the RBA has more cuts in the bag before asset purchases are formally announced, while they would obviously like the government to do more on a fiscal note. However, if the market sees the need for more extreme measures they will go after the RBA. The AUD is arguably one to watch in 2020 and tactically feels like there are significant downside risks notably against the GBP.

The material provided here has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such is considered to be a marketing communication. Whilst it is not subject to any prohibition on dealing ahead of the dissemination of investment research we will not seek to take any advantage before providing it to our clients.

Pepperstone doesn’t represent that the material provided here is accurate, current or complete, and therefore shouldn’t be relied upon as such. The information, whether from a third party or not, isn’t to be considered as a recommendation; or an offer to buy or sell; or the solicitation of an offer to buy or sell any security, financial product or instrument; or to participate in any particular trading strategy. It does not take into account readers’ financial situation or investment objectives. We advise any readers of this content to seek their own advice. Without the approval of Pepperstone, reproduction or redistribution of this information isn’t permitted.