- English

- 中文版

Analysis

There are two areas to consider when it comes to real estate – residential, and commercial. The latter remains under considerable pressure, not only from tighter monetary policy, but also as the broader macroeconomy continues to adjust to working habits in the post-covid world, with remote/hybrid working continuing to depress office occupancy rates, while also exerting pressure on city centre businesses reliant on worker traffic, such as restaurants and cafés.

It is, however, the residential real estate market that is more likely to prove a tradeable theme, particularly in the FX space. Several G10 economies display similar characteristics, whereby house prices have rapidly increased in recent years, a mortgage cliff (where fixed rate deals are being refinanced at rates double, or more, than the original loan) is rapidly approaching, and where the risk of both substantial delinquencies and a sharp fall in house prices is high. Australia, Sweden, and the UK would be the primary economies falling into this camp.

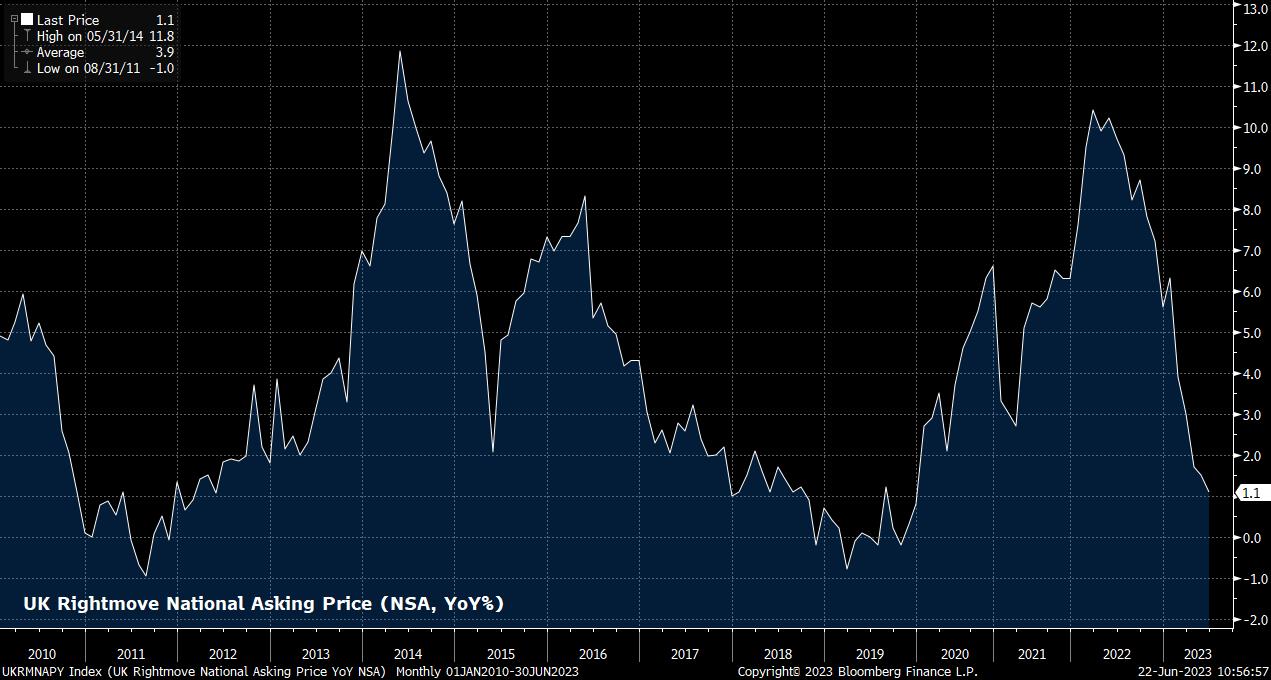

In the case of the UK, the situation is particularly stark, and a good example of both how lagged the effects of policy tightening can be, and what may develop in other developed economies. Around 2mln fixed rate mortgages, with rates below 2.5%, will roll off between now and the end of 2024; with the current 2-year fix averaging north of 6%, many of these borrowers will see interest costs treble overnight. The rate rise itself, however, has not been overnight, with the BoE having been tightening policy since December 2021, though it is only now that the impact of said hikes is feeding through into the economy.

Perhaps more importantly, not only has the impact of tightening been delayed, it is also likely to be more prolonged, given the increasing tendency to fix mortgage rates for a longer period of time – the majority of fixed rate loans extended YTD have been for a tenor of at least 5 years. This, consequently, will mean that when the BoE eventually begin to loosen policy – at some point in the future – the impact of said cuts will not be immediately felt, thus leading to the present level of rates acting as an economic drag for some time to come.

This makes a structural bull case for the GBP rather tough to come by, especially considering that the bulk of this mortgage refinancing will come later this year, leading to a significant drop in disposable income, likely denting discretionary spending, as consumers tighten their belts. While this will, hopefully, have a much-needed disinflationary impact on the economy, it will likely serve to deepen the stagnation that already plagues the UK.

_2023-06-22_11-05-08.jpg)

A similar trend is likely to be seen in other economies, and currencies, with similar characteristics – such as the SEK and the AUD, where it is noticeable that both central banks have been almost as reluctant as the Bank of England to tighten policy, lest it have a significant detrimental impact on their respective real estate markets.

Outside of the FX space, there are other ways for traders to gain exposure to the broader real estate theme. The iShares US Real Estate ETF is one that could be considered, and a fund which exhibits broader investor angst over the state of the sector, given its considerable underperformance compared to the broader S&P 500 YTD.

Related articles

The material provided here has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such is considered to be a marketing communication. Whilst it is not subject to any prohibition on dealing ahead of the dissemination of investment research we will not seek to take any advantage before providing it to our clients.

Pepperstone doesn’t represent that the material provided here is accurate, current or complete, and therefore shouldn’t be relied upon as such. The information, whether from a third party or not, isn’t to be considered as a recommendation; or an offer to buy or sell; or the solicitation of an offer to buy or sell any security, financial product or instrument; or to participate in any particular trading strategy. It does not take into account readers’ financial situation or investment objectives. We advise any readers of this content to seek their own advice. Without the approval of Pepperstone, reproduction or redistribution of this information isn’t permitted.