- English

- 中文版

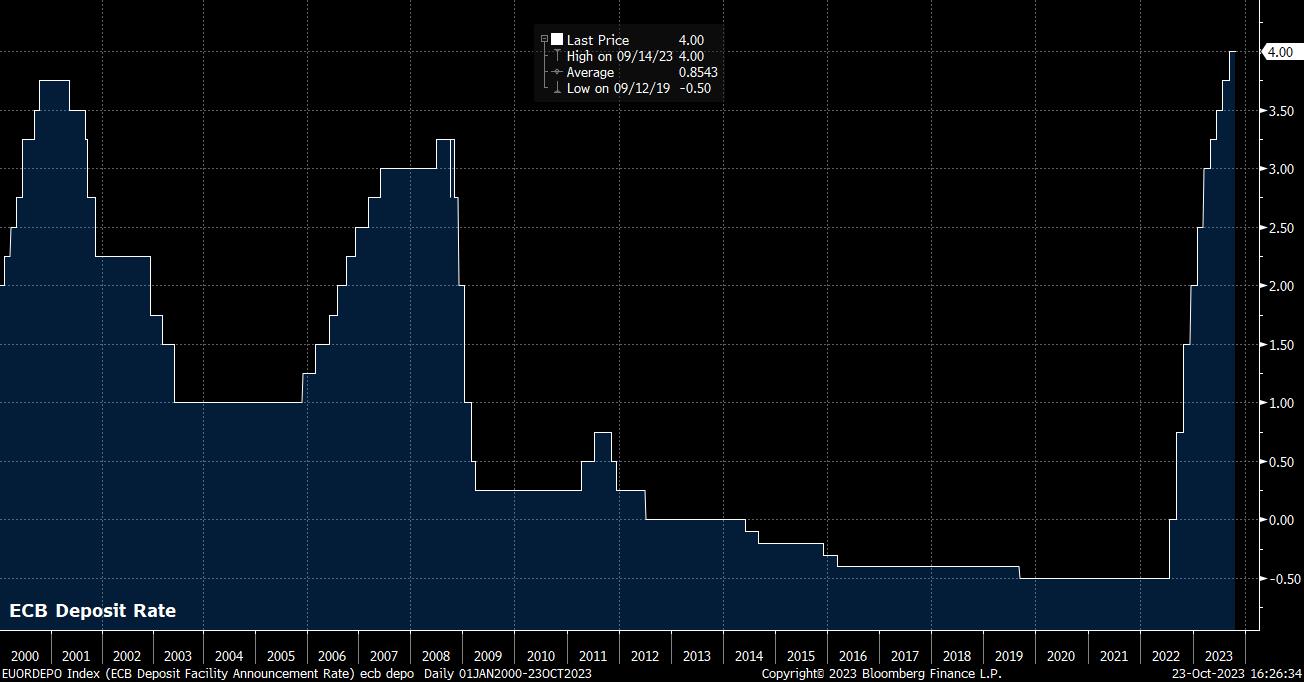

As noted, the deposit rate is set to be maintained at a record high 4.00% this time around. In fact, money markets price next to no chance of any move, nor any further tightening, evidencing a firm belief that the terminal rate has already been reached.

Interestingly, however, OIS continues to price the first deposit rate cut for July 2024, though does see a roughly 80% chance that such a 25bp cut could come as soon as next June. This seems at odds with the Governing Council’s current guidance that rates will have to remain at “sufficiently restrictive levels for as long as necessary”. A repeat of this guidance seems nailed-on for this week’s decision, along with a reiteration of the commitment to set policy in a data-dependent manner, both in terms of the level rates reach, and the duration rates spend at said level.

This meeting gives policymakers an opportune moment to pause, and take stock of recent economic developments, while retaining the optionality to raise rates further if inflation were to rear its head once more.

On the subject of economic developments, incoming inflation data has begun to move in a more promising direction for the ECB. Both headline and core CPI slipped back under 5% YoY in September, the headline measure touching a 2-year low, while rapidly falling producer prices point to disinflation continuing in the months ahead. Risks do, however, remain tilted to the upside, with the labour market remaining relatively tight across the bloc, in addition to geopolitical developments in the Middle East posing the risk of the bloc having to grapple with an energy supply shock for the second successive winter.

Of course, the geopolitical situation remains fluid, and uncertain, with it still being too early to gauge the macroeconomic impacts of the current conflict. Nevertheless, while risks to the ECB’s inflation projections, which already foresee CPI remaining above the 2% target through to the end of 2025, remain tilted to the upside, growth risks facing the bloc continue to tilt to the downside.

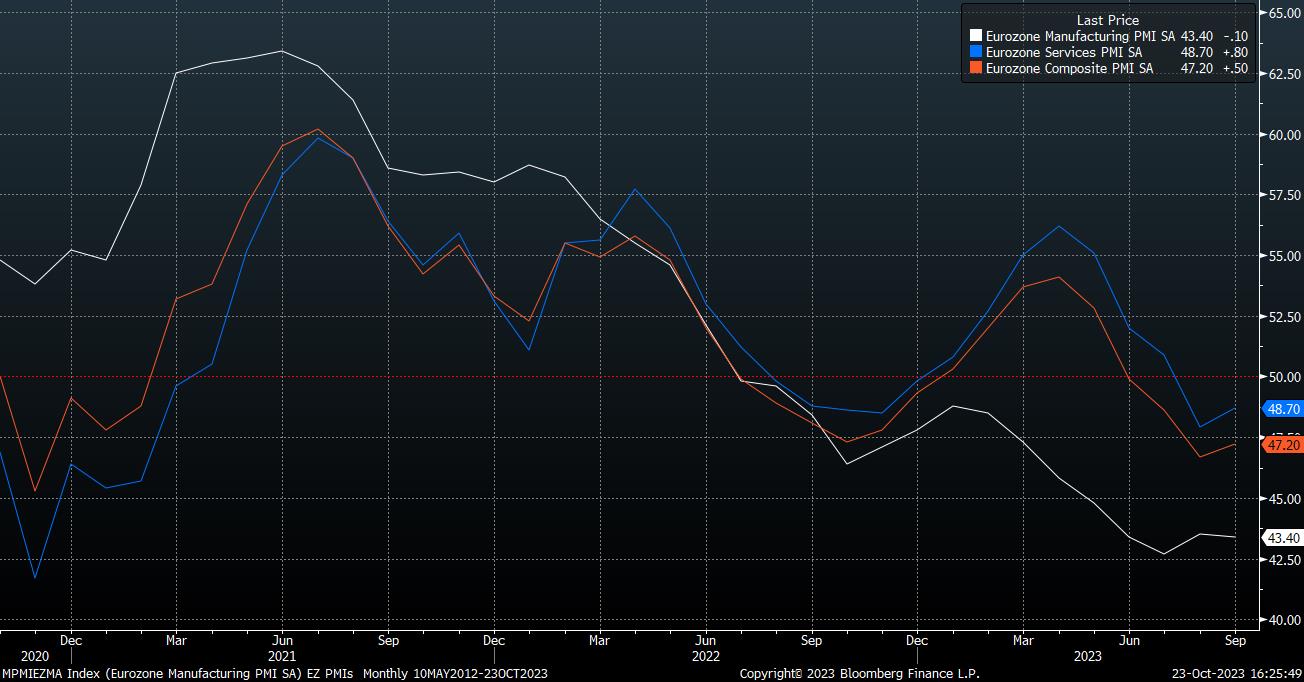

Leading indicators continue to imply a contraction in both the manufacturing and services sectors, with September’s PMI surveys remaining below the key 50 mark, while October’s data – due two days ahead of the ECB’s decision – is set to paint a similar picture. Of course, rising geopolitical tensions, along with the continued lack of a concrete economy recovery in China, are also posing headwinds.

It is against this backdrop that even the Governing Council’s hawks are likely content to sit on their hands this month. Nevertheless, some discussion is likely to take place around some of the more complex areas of the ECB’s toolkit – namely minimum reserve balances, and the reinvestment of maturing PEPP securities – though decisions on either are unlikely until the final meeting of the year in December.

In terms of minimum reserves, which are now remunerated at 0% since July, rather than the deposit rate as previously, it seems likely that policymakers will seek to raise minimum reserve requirements in the near future, thereby requiring eurozone banks to hold additional capital with the central bank. Such a decision, likely in December, following discussion this month, seems almost entirely driven by the ECB’s desire to save on net interest payments, rather than any specific monetary policy or financial stability rationale.

In any case, such a move is likely to be met with further scorn from eurozone banks, while also having a detrimental impact on eurozone bank stocks, which have endured a poor run of late.

On the latter matter, of tweaking the plan to halt reinvestments of maturing PEPP securities at the end of 2024, any chance of an imminent decision here has been dented by recent market moves.

The rampant DM debt sell-off, led by Treasuries, but impacting the eurozone in a similar manner, makes now an inopportune moment to be announcing a faster pace of balance sheet run-off. Furthermore, renewed concerns about debt sustainability within the eurozone, particularly when it comes to Italy, with the BTP-Bund spread nearing 200bp once more, will likely make reaching a consensus on this matter within the Governing Council difficult at this stage.

On the whole, with few policy changes or concrete guidance shifts likely to be produced by the October meeting, it may prove to be one that has little, if any, prolonged impact on the EUR. In fact, ahead of the decision, one-week implied EUR/USD volatility remains below the 20th percentile of its 52-week range, pointing to a move of less than a big figure over the course of the next five trading days (with 1 standard deviation of confidence).

In terms of levels, 1.0650 remains the key upside level that EUR bulls will have on the radar, particularly with the common currency coming into the ECB meeting on the back of its best week since July; the 50-day moving average, which spot hasn’t traded above since August, sits just above at 1.0685.

_eurusd_mb_2023-10-23_16-24-29.jpg)

To the downside, the 1.05 figure remains key psychological support, with a closing break below said level likely opening the door to a retest of the prior 1.0450 low, before a further decline towards 1.0355. Currently, the balance of risks would point towards downside being the more likely direction of travel.

Related articles

.jpg?height=420)

.jpg?height=420)

The material provided here has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such is considered to be a marketing communication. Whilst it is not subject to any prohibition on dealing ahead of the dissemination of investment research we will not seek to take any advantage before providing it to our clients.

Pepperstone doesn’t represent that the material provided here is accurate, current or complete, and therefore shouldn’t be relied upon as such. The information, whether from a third party or not, isn’t to be considered as a recommendation; or an offer to buy or sell; or the solicitation of an offer to buy or sell any security, financial product or instrument; or to participate in any particular trading strategy. It does not take into account readers’ financial situation or investment objectives. We advise any readers of this content to seek their own advice. Without the approval of Pepperstone, reproduction or redistribution of this information isn’t permitted.