- English

- 中文版

The Daily Fix: Looking for new highs in Asian equity markets

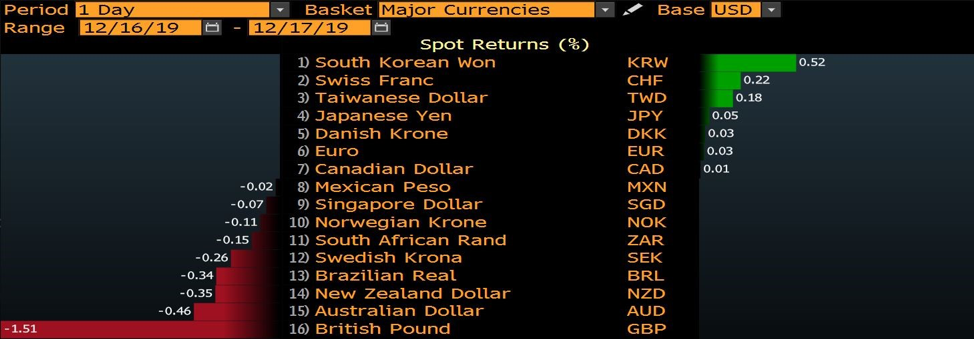

"(Source: Bloomberg)"

A 1.5% drop in GBPUSD takes the year-to-date gains to 2.9%, subsequently promoting the MXN and CAD as the star major currencies in 2019. Also, consider Friday’s blockbuster UK election exit poll saw cable rally hard from 1.3184 into 1.3514 in a 30-minute period, and since then the price has all but give up those gains and more, hitting the 1.31 handle at 03:48 AEDT. A far cleaner position is now seen in GBP positioning, with a decent flush out of overextended longs, and this is true of the GBP crosses with EURGBP gaining 1.7% - its best one-day gain since 15 November 2018.

Is this the time to wade back into GBP longs?

Perhaps, but it’s a brave call here and I’d want to see more conviction in the price action from the GBP bulls, as the market still needs to find a consensus on how the ‘Transition Period’ plays out and if this renewed threat of a no-deal Brexit is a true risk.

Boris Johnson has seen modest success utilising the threat about taking the UK out of the EU without a deal in his prior negotiating tactics and he’ll continue using this threat as a weapon. So, for anyone thinking 2020 was going to be smooth sailing for the GBP, with Boris getting his deal through the Commons, business confidence returning as the Transition Period is extended by two years, and the BoE turning hawkish at the margin (from late Q2/early Q3) has been given a wake-up call. Traders are once again going to have to work for their profits in this currency.

GBPUSD 1-month implied volatility (IV) has pushed a tad higher into 8.4775%, although, this isn’t overly high and doesn’t scream of expected oversized moves just yet. For context, this IV is the 50th percentile of the two-year range.

AUDUSD vols into the lower bounds

AUDUSD 1-month implied volatility sits at 5.79%, which is the 2nd percentile of the two-year range, even if AUDUSD found a steady stream of sellers into 0.6838. All is well, all is calm in AUD land, it seems, and while the RBA opened the door to a rate cut in the 4 February meeting, vols have followed that of CNH vol, which has been sold with the Chinese committing to keeping a stable yuan. For me, IV has huge implications for how much risk we’re prepared to accept and our position sizing.

The playbook for the AUD is fairly straightforward here. A poor jobs report tomorrow (consensus 15k jobs, u/e rate unchanged at 5.3%) would lift expectations of a cut in February to 70%, from current pricing of a 55%. Expectations would then likely stay at these levels unless we saw signs of life in the upcoming retail sales (10 January), and Dec jobs report (23 January).

Even then, with the government’s recent MYEFO basically telling FX traders that any stimulus is coming from the RBA and not at a fiscal level, the fact the RBA minutes said they can “provide further stimulus to the economy if required” has raised expectations the cash rate could be at 50bp soon.

AUDNZD looks interesting, and tactically I would be playing this in small size (initially) from the short side, with stops above 1.0490, with a view to add on a daily close through 1.0400.

The Riksbank to set a precedent

Given today is the last Daily Fix until mid-January, I want to keep an eye on the Skandies, notably EURSEK and NOKSEK, as there’s plenty of buzz about the Swedish Riksbank hiking rates tomorrow, subsequently, taking interest rates out of negative territory and the blueprint this sets for the likes of the ECB and BoJ and other central banks who have negative interest rates and seeing signs of economic stabilisation. Consider the Swedish swaps market has 15bp of hikes priced through the coming 12 months and it’s clear that traders expect a one-and-done view on hikes - so in theory, the hike itself shouldn’t be a volatility event, as the market expects the bank to make it clear that this is not the start of a tightening cycle.

Moves elsewhere

Outside of FX land, it’s been a fairly quiet session, with the S&P 500 changed, small caps (i.e. Russell 2000) +0.4%, on volumes pretty much in-line with the 30-day average. US Treasury’s have moved up smalls (UST 10s are +1bp), with WTI crude +1.1%, while copper and gold are unchanged. Credit markets have been getting headlines, reinforcing the notion that shorting US equity indices into year-end is a tough trade - whether we’re looking at higher quality investment-grade or even junk-rated debt, spreads or even the cost of hedging credit risk (through credit-default swaps) are telling us that appetite to be long risk is still very high.

(IG CDX - HY CDX)

That could change in 2020, as there has been such incredible debt accumulation in the lower-rated corporate bond space, that this level of enthusiasm from investors to absorb such debt issuance has made the space frothy. I won’t be betting against this momentum at this stage, as that will require a more recessionary environment and the market to feel central bank stimulus will fail to offset a tougher economic climate. We are clearly not there yet, in fact, the UST 2vs 10s Treasury yield curve is just 6bp from year-to-date highs, while the copper/gold ratio pushes higher and sits at the strongest levels since July.

(US 2s vs 10s curve)

We turn to the Asian session open and we look to see if the bulls can reassert their dominance in what is to be a flat open. The ASX 200 gets central focus with the cash open likely to be unchanged, but in this positive risk environment, there is some belief that the buyer will step in for a re-test of the all-time high of 6893.70 (set on 29 November). The Hang Seng should open modestly stronger and will look to test the swing high of 27900, while the Nikkei 225 will also open unchanged, with the trend clearly bullish – that said, there is a fairly punchy gap to close into 23468.

As mentioned, this is the last Daily Fix until 13 January, so I wish everyone a good festive period and good luck to all those trading through the period.

The material provided here has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such is considered to be a marketing communication. Whilst it is not subject to any prohibition on dealing ahead of the dissemination of investment research we will not seek to take any advantage before providing it to our clients.

Pepperstone doesn’t represent that the material provided here is accurate, current or complete, and therefore shouldn’t be relied upon as such. The information, whether from a third party or not, isn’t to be considered as a recommendation; or an offer to buy or sell; or the solicitation of an offer to buy or sell any security, financial product or instrument; or to participate in any particular trading strategy. It does not take into account readers’ financial situation or investment objectives. We advise any readers of this content to seek their own advice. Without the approval of Pepperstone, reproduction or redistribution of this information isn’t permitted.