- English

- 中文版

US equity and index options expiry may have played a part in the equity drawdown, with dealer’s net short gamma and delta hedging through shorting S&P500 futures and single stock names. Let’s see how options dealers/market makers deal with this inventory of short positioning/hedges this week, as it may be unwanted - suggesting risk that they buy back short S&P500 futures hedges (to close), which could cause an early relief rally in equity.

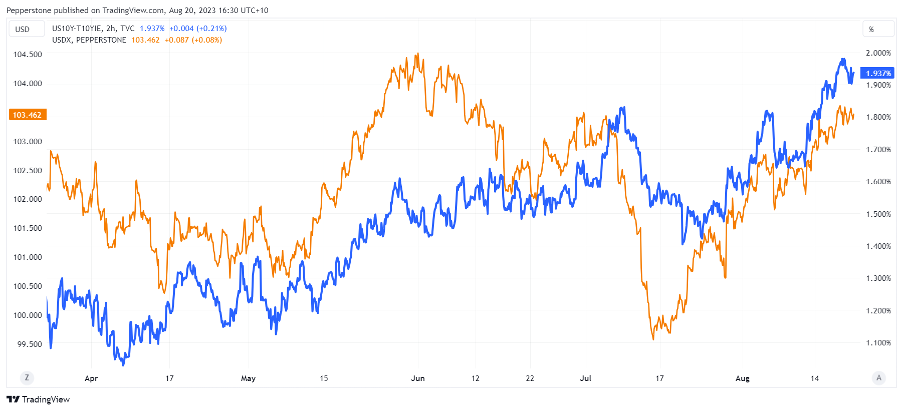

Positioning will play a huge part this week, and it wouldn’t take much to see US real rates a touch lower, with the USD following in its wake.

As the new trading week cranks up, news flow on China will drive and should the HK50 and CNH find further selling interest, then I’d aligned with a bias to look at short GER40 trades. The China property sector remains the elephant in the room, with the market finding little tangible fiscal support to reprice risk higher – the price action in the HK50 reflects that, with rallies quickly sold into. Weekend news that the PBoC and financial regulator are leaning on banks to increase lending is a positive step, but we question whether there is the demand to increase volume.

We get PMI data out throughout the week, but as the week rolls on the attention should turn to Jackson Hole, where Jay Powell takes centre stage. While this forum has been the setting for some bold changes to monetary policy in years gone by, it doesn’t feel like this time around we’ll be treated to such action. The USD remains front and centre this week – biased long, I acknowledge positioning is rich and could easily be vulnerable to profit taking into Powell’s speech.

USD (orange) v US 10yr real rates (blue)

The marquee data to navigate:

- China loan prime rate decision (21 Aug 11:15 AEST) – after the PBoC surprised the market and eased the Medium-Lending Facility last week, we should see the PBoC ease the 1- and 5-year Prime lending rate by 15bp respectively. Unless we see the Prime Rate left unchanged, Chinese equity markets will likely overlook any policy easing here and funds should continue to shy away from HK50, CHINAH, and CN50 longs. USDCNH finds support below 7.3000, but few are buying yuan with conviction other than to cover yuan shorts.

- Eurozone manufacturing and services PMI (23 Aug 1800 AEST) – the market eyes the manufacturing index at 42.6 (from 42.7) and services at 50.5 (50.9). A weaker services PMI, especially if the data prints below 50 (the expansion/contraction line) and we could see better EUR sellers, with the GER40 eyeing a break of the July lows of 15,500. Tactically warming to EURCAD shorts.

- UK manufacturing and services PMI (23 Aug 18:30 AEST) – the market looks for manufacturing to come in at 45 (45.3) and services at 50.8 (51.5). GBP – the best performing major currency last week - could be sensitive to the services print.

- US S&P Global manufacturing and services PMI (23 Aug 2345 AEST) – with much focus on China’s markets, US real rates and Jackson Hole, there is less concern about US growth metrics. As a result, the outcome of this may have a limited impact on the USD – it is still a risk to have on the radar.

Jackson Hole Symposium – Fed chair Jay Powell will be the highlight of the conference (speaks Sat 00:05 AEST) – again, it’s still premature for Powell to declare victory in the Fed’s inflation fight and will likely emphasise there is still more work to be done. He may also spend time exploring a higher for longer mantra (for interest rates), with a focus on where they are modelling the neutral fed funds rate; possibly one for the PhDs and academics. Powell should re-affirm his view that rate cuts are not in their immediate thinking.

From a risk management perspective, I am sensing Jackson Hole/Powell’s speech to be tilted on the hawkish side, and therefore modestly USD positive. Although given the bull run in the USD one could argue a hawkish Powell is largely priced.

Other Jackson Hole speakers:

- Fed members Goolsbee and Bowman (23 Aug 05:30 AEST)

- Fed member Harker (25 Aug 23:00 AEST)

- ECB president Lagarde (26 Aug 05:00 AEST)

BRICS Summit in South Africa (Tuesday and Wednesday) – It’s hard to see this as market moving and a risk event for broad markets. However, with BRICS countries (Brazil, Russia, India, China, and South Africa) accounting for 32% of global GDP and some 23 countries wanting to join the union, there will be increased focus on their expansion plans. Some have linked the BRICS to an acceleration of global de-dollarization, and while a global reliance on the USD will likely fall over time, the movement is glacial. A common currency for this union – while possibly getting headlines at this summit - is not something that seems viable anytime soon.

Key corporate earnings:

US - Nvidia report earnings (aftermarket) – many will recall the 24% rally in the share price in Q1 earnings (in May) and hope for something similar. Given the incredible run and heavy positioning, it may need something truly inspiring to blow the lights out. The market prices an implied move on earnings is 10.2%, so one for those who like a bit of movement in their trading.

Australia – 68 ASX200 co’s report, including – BHP, Woodside Petroleum, Qantas, Northern Star and Wesfarmers

Related articles

_(6).jpg?height=420)

The material provided here has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such is considered to be a marketing communication. Whilst it is not subject to any prohibition on dealing ahead of the dissemination of investment research we will not seek to take any advantage before providing it to our clients.

Pepperstone doesn’t represent that the material provided here is accurate, current or complete, and therefore shouldn’t be relied upon as such. The information, whether from a third party or not, isn’t to be considered as a recommendation; or an offer to buy or sell; or the solicitation of an offer to buy or sell any security, financial product or instrument; or to participate in any particular trading strategy. It does not take into account readers’ financial situation or investment objectives. We advise any readers of this content to seek their own advice. Without the approval of Pepperstone, reproduction or redistribution of this information isn’t permitted.