- English

- 中文版

A Turning Point in the Australian Economy and a Possible Final RBA Rate Hike

Summary

• RBA expected to hike 25bp to 4.35%, with ~76% probability priced • Inflation remains above target, forcing a tightening bias

• Growth expected to peak and slow into year end • Fiscal support to ease, adding pressure to the outlook

• Debate builds on whether this is the final rate hike

• AUD implications likely more pronounced on cross rates

A Turning Point in the Australian Economy

It is becoming clear that we have hit a turning point and an inflection point in the Australian economy, with risks now firmly skewed towards slower growth into year end.

One could argue that ASX200 domestic cyclical equities have sensed this for some time. While this has also been influenced by RBA rate hikes, higher costs of capital, and cost of living pressures driven by energy and food prices, the underperformance in ASX-listed retailers and banks suggests investors have already priced in this dynamic impacting future earnings.

RBA Meeting and Rate Hike Expectations

The RBA meets on Tuesday, and we will learn more about how it views the evolving dynamics between above target inflation and a slowdown in the domestic economy. This will come through its statement and Governor Bullock’s press conference shortly after, and the market will react accordingly.

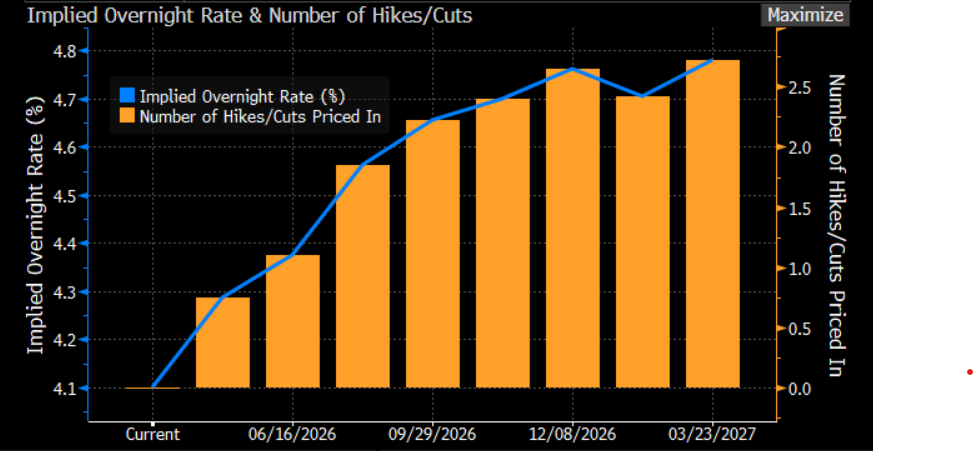

The RBA will most likely raise the cash rate by 25 basis points to 4.35%. This is currently priced and implied at a 76% probability in AUD interest rate swaps, with 20 out of 21 economists also calling for that hike.

Inflation Pressures Driving Policy

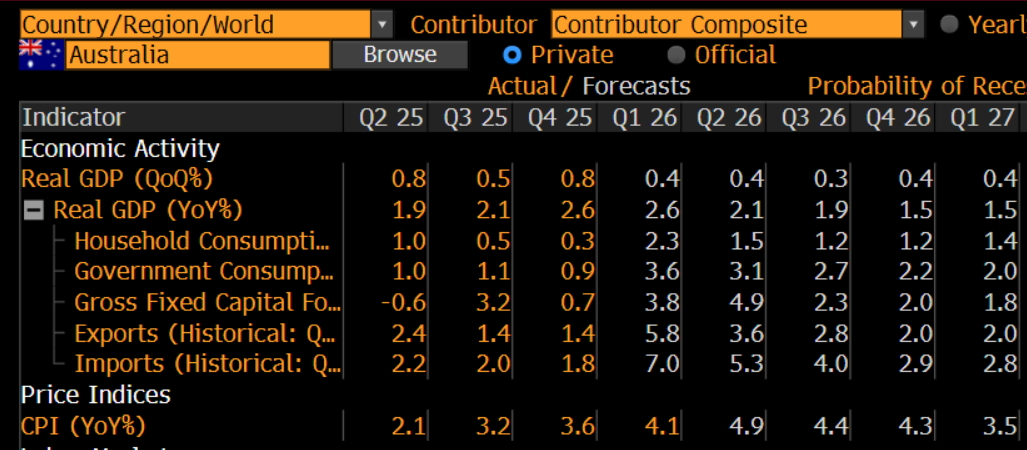

The RBA’s hand will be forced by recent inflation dynamics, with March headline inflation at 4.6%, the highest since 2023, and Q1 trimmed mean inflation coming in 30 basis points above the RBA’s 2 to 3% target. Goods inflation is notably running at 5.2% year on year.

It will be a close call though. and as seen in the March meeting, the vote split was five in favour of a hike and four for a hold, and we may see a similar split this time.

Growth Outlook and RBA Concerns

However, the RBA’s statement should highlight increased concern around consumption patterns and a subsequent slowdown into year end. This is something the RBA has already modelled in its recent Statement on Monetary Policy, where growth was projected at 1.8% in the December half, falling to 1.6% in the first half of 2027.

Looking ahead, on 3 June we get the Q1 GDP print. Economists expect headline GDP to remain at 2.6%, unchanged from Q4. Household consumption is expected to build to 2.3%, with government consumption at 3.6%. However, this will almost certainly mark the peak in Australia’s growth rate.

Economists expect household consumption to moderate through the quarters to 1.2% by December, while government consumption is expected to slow to a 2.2% growth rate by year end. This would bring real GDP growth down to around 1.5% at the headline level by December.

Is This the Final Rate Hike?

Importantly, interest rate swap pricing implies a further 25 basis point hike could come in the August or September RBA meeting. However, there should be real debate as to whether that happens.

The key question is whether a cash rate of 4.35%, which would take the RBA’s policy rate back to levels seen post COVID and before the easing cycle began, will mark the final hike in this cycle.

Federal Budget and Fiscal Policy

We also have the Federal Budget on 14 May. Much of this has already been reported and debated in the media, so there should be few surprises.

The market is focused on the level of fiscal support. While government spending will remain supportive, it is likely to be reduced, with a focus on increasing housing supply and reducing support for investors.

A potential surprise could come if changes to capital gains tax deductions or the speculated tweaks to negative gearing are applied retrospectively rather than being grandfathered, which is currently the consensus expectation.

The combination of a cash rate at 4.35%, modestly reduced fiscal support, a higher cost of capital, and ongoing constraints in the Strait of Hormuz, which could become more problematic for businesses, all adds conviction to the view of a moderation in Australia’s growth rate.

The key question then becomes what happens on the inflation front. This could see the term stagflation used more frequently, even if in reality the dynamic remains manageable and not a major risk to Australian asset pricing.

Implications for the Australian Dollar

For the AUD, a cash rate of 4.35% held for a period, alongside slowing growth, will have implications. This may be less evident against the US dollar, which tends to be driven by global risk dynamics, but more pronounced against cross rates.

While Australia’s growth is slowing, it is important to consider this on a relative basis. Will Europe, the UK, Japan, and other developed market economies also slow into year end, or will they see modest improvement? Relative growth dynamics will be key in driving capital flows and currency movements, alongside market pricing of forward interest rate expectations.

Final Thoughts

In the near term, we should expect the RBA to hike the cash rate next week, followed by a largely unsurprising budget. However, the risks to Australia’s growth outlook are now clearly skewed to the downside.

As such, the probability of one final rate hike appears to be the most likely outcome.

The material provided here has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such is considered to be a marketing communication. Whilst it is not subject to any prohibition on dealing ahead of the dissemination of investment research we will not seek to take any advantage before providing it to our clients.

Pepperstone doesn’t represent that the material provided here is accurate, current or complete, and therefore shouldn’t be relied upon as such. The information, whether from a third party or not, isn’t to be considered as a recommendation; or an offer to buy or sell; or the solicitation of an offer to buy or sell any security, financial product or instrument; or to participate in any particular trading strategy. It does not take into account readers’ financial situation or investment objectives. We advise any readers of this content to seek their own advice. Without the approval of Pepperstone, reproduction or redistribution of this information isn’t permitted.