- English

- 中文版

The case for the FOMC to deliver a rate cut, sooner rather than later, continues to grow, resting on three main pillars:

- Increased disinflation confidence

- Cracks emerging in the labour market

- A continued rise in the real fed funds rate

Let’s take each in turn.

On the inflation side of proceedings, while one must acknowledge that the June CPI report may throw a ‘spanner in the works’, it is clear that progress continues to be made back towards the 2% target. Said progress can be judged on numerous metrics, though most, if not all, paint a relatively positive picture:

- Core CPI, at 3.4% YoY in May, is at its lowest level in three years

- YoY ‘Supercore’ CPI (core services ex-housing) fell in May, to 4.8%, for the first time this year

- Core PCE, the Fed’s preferred inflation gauge, at 2.6% YoY, sits at its lowest since April 2021

- Core PCE, on a monthly basis, at 0.08% in May, sits at its lowest since all the way back in November 2020

- Goods deflation has continued to deepen, with core goods CPI falling at its fastest pace in over a decade in May, while core services CPI fell – on an annual basis – at its most rapid rate in three months

Clearly, the job is not done in terms of returning to 2%. However, as is always the case, one must acknowledge that monetary policy works with 'long and variable lags’, often between 18 and 24 months. Hence, action now will only be fully felt within the economy by the middle of 2026.

This explains why the FOMC’s guidance has been that the Committee are seeking ‘confidence’ in inflation moving towards the 2% target, rather than achieving it outright. Waiting until the target is achieved would likely result in a significant inflation undershoot, as normalisation would begin much too late.

The balance of the above data should provide enough confidence that the inflationary beast has been slain, though holding out until the end of summer for a handful more data points is unlikely to do much harm. It is, perhaps, natural for policymakers to want to err on the side of caution in determining the timing of the first cut, with the post-covid ‘transitory’ inflation disaster still fresh in most minds.

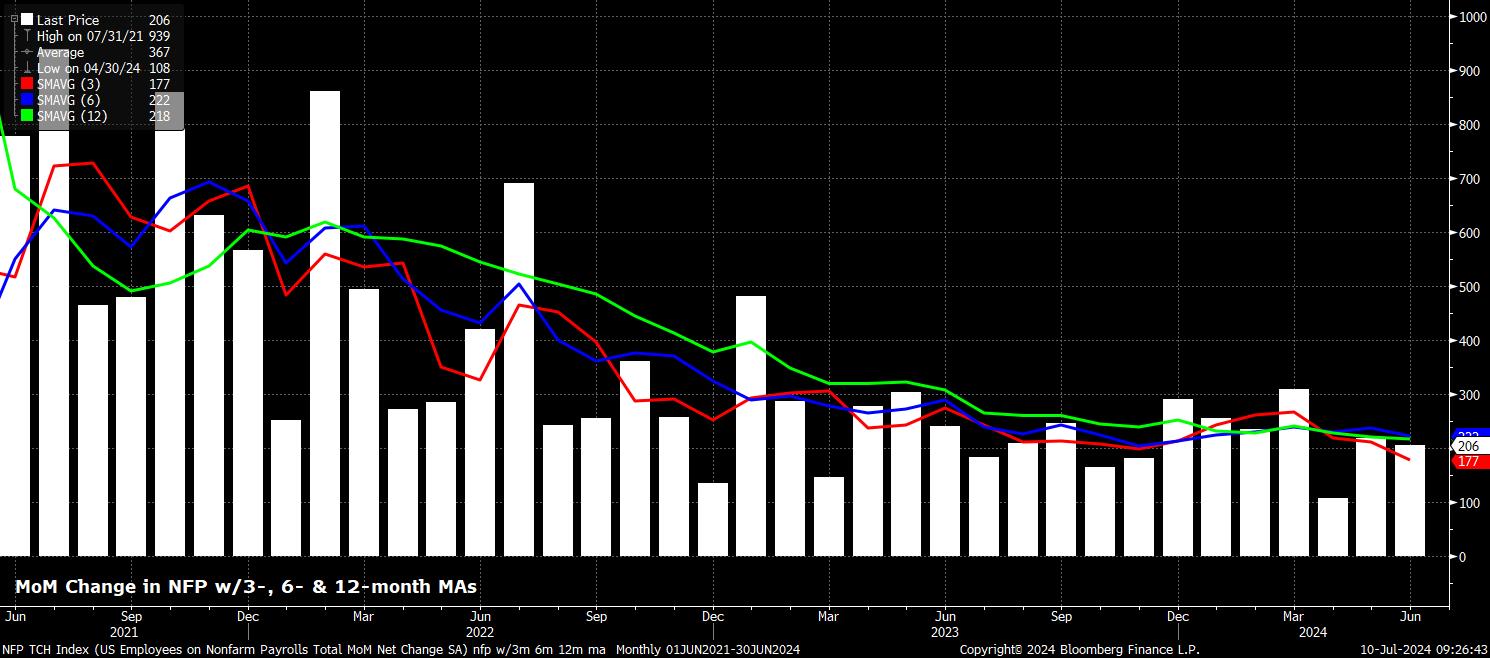

Meanwhile, on the labour market, cracks continue to emerge.

While having beat expectations, with nonfarm payrolls having risen +206k in June, the print came with a chunky net -111k revision to the prior two months’ worth of data. Together, this has seen the 3-month average of job gains slip to +177k, the lowest level since February 2021, and well below the 225k – 250k ‘breakeven’ pace of job gains required for employment growth to keep pace with the increasing size of the labour force.

Similar signs of fragility emerge if one looks at the household survey.

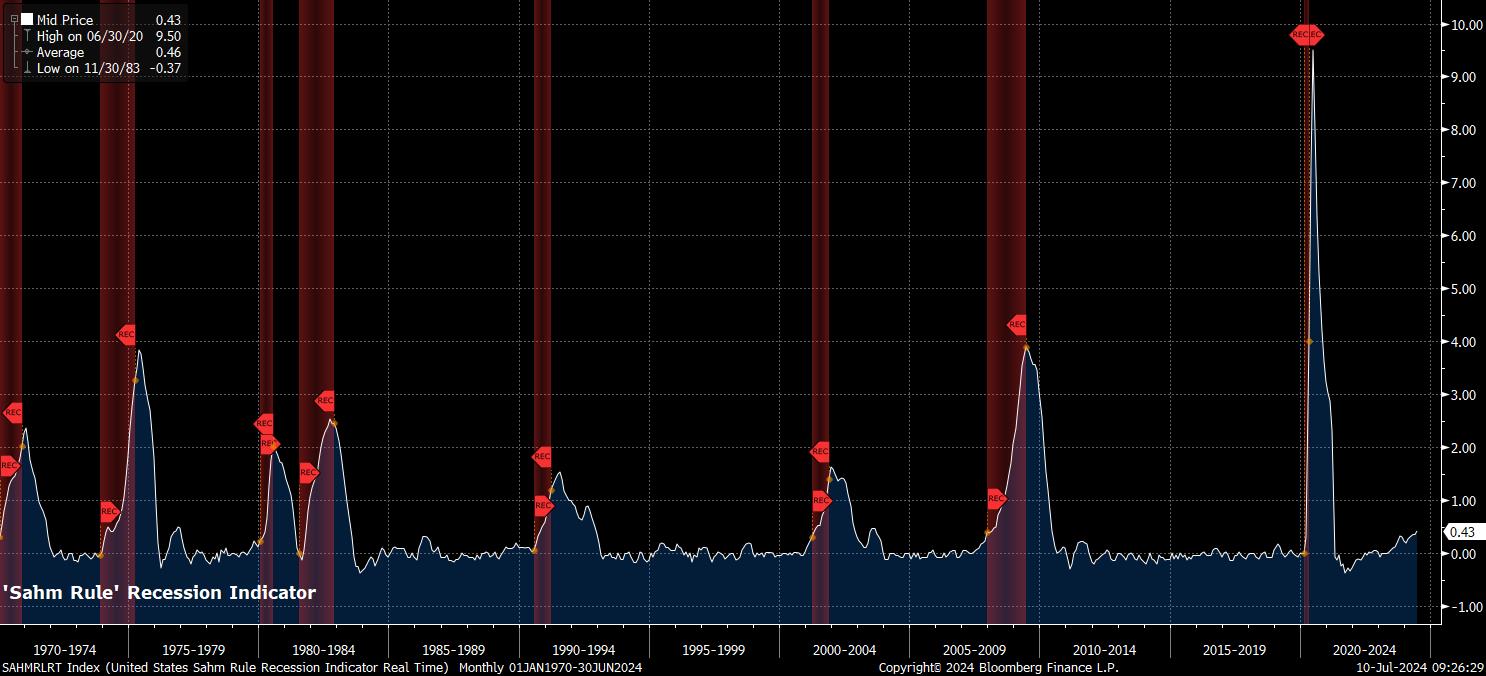

Here, although participation did rise 0.1pp to 62.6% last month, unemployment also rose, to 4.1%, the highest level since November 2021. Not only does this represent the third consecutive month in which joblessness has risen, the data also puts the economy just 0.07pp away from triggering the so-called ‘Sahm Rule’ – a rule which has previously heralded the start of a recession (every one since 1970), stating that such a slowdown has begun when the 3-month average of the unemployment rate rises 0.5pp above its 12-month low.

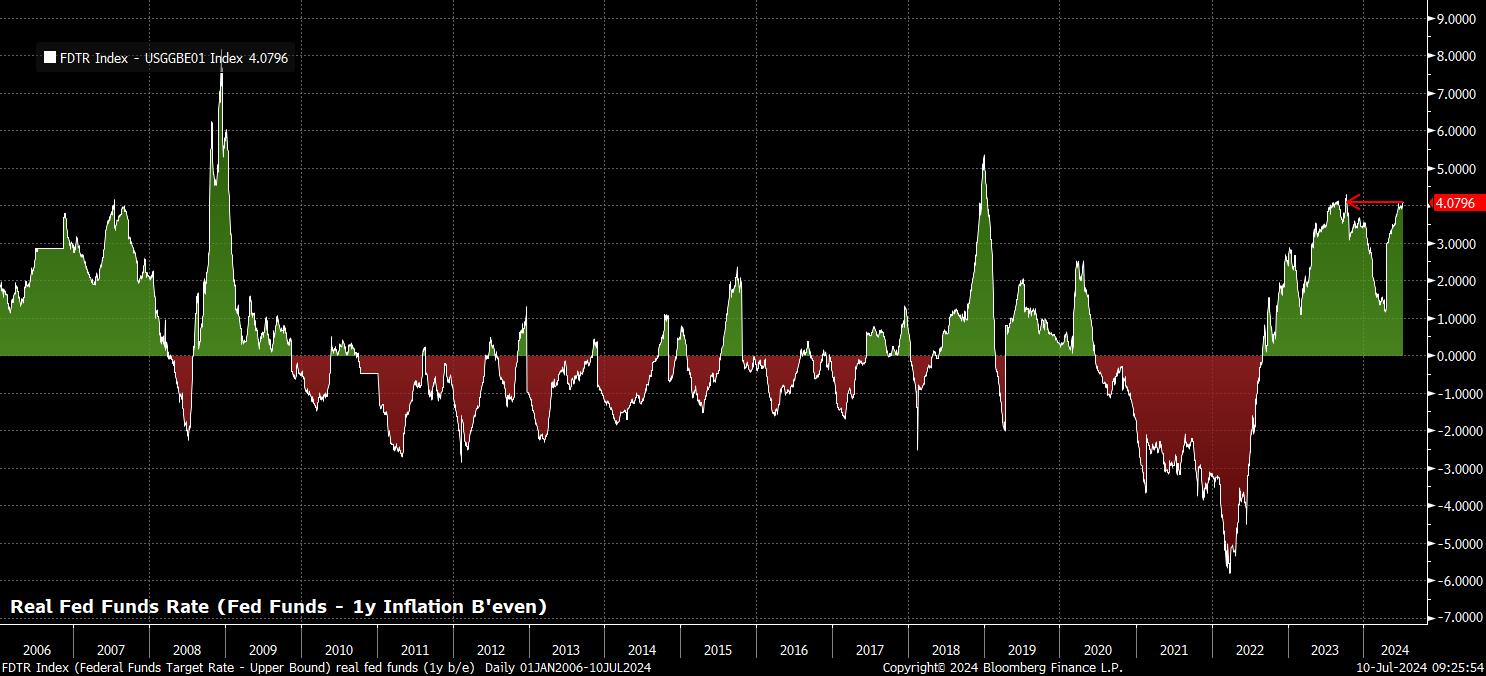

The third pillar is apparent when one looks at the relative policy stance.

As has been discussed in these pages at some length, by holding the fed funds rate steady, as inflation continues to fade, there is a mechanical tightening of the overall policy stance, as the real (inflation adjusted) fed funds rate continues to move higher.

While there are many metrics that one can use, and many appropriate inflation measures by which one can discount the fed funds rate to obtain a ‘real’ reading, Chair Powell’s favoured metric is as followed – to subtract from the fed funds rate the one-year inflation breakeven. Using such a calculation shows that the real fed funds rate is now north of 4% once more, and in fact stands at its highest level since last October.

Taking these three factors together helps to explain the subtle, but significant, dovish tweaks that Chair Powell has appeared to make to his language in recent appearances.

At the ECB’s Sintra conference at the start of the month, Powell flagged the ‘two-sided risks’ that the FOMC now face, while also flagging that the US economy appears to be back on a ‘disinflationary path’. Powell then went a touch further in remarks to the Senate Banking Committee, as part of the semi-annual ‘Humphrey Hawkins’ testimony, noting that the labour market appears to be ‘fully’ back in balance, that the economy is no longer ‘overheated’, and that policymakers can no longer focus ‘solely’ on inflation.

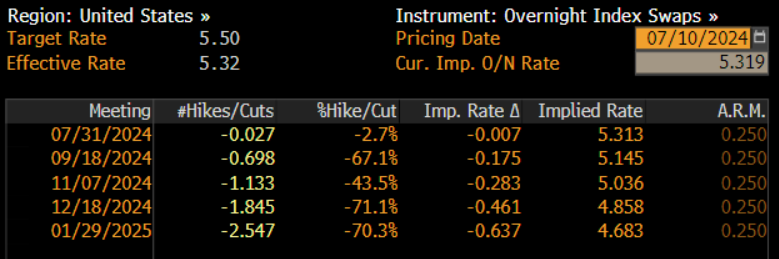

Comments of this ilk appear to further open the door to a cut in September providing, of course, that incoming data continues to behave itself. The USD OIS curve currently implies around a 70% likelihood of such a cut, while discounting 46bp of easing by the end of the year, with a second 2024 cut likely to be delivered in December.

Such an outlook is, naturally, supportive of risk sentiment more broadly – not only is the ‘Fed put’ still in place, with policymakers displaying a clear desire, and readiness, to ease policy as and when necessary, such easing is likely to be delivered in relatively short order. Equities, then, should continue to move to the upside over the medium-term, with any dips continuing to represent buying opportunities.

Related articles

.jpg?height=420)

The material provided here has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such is considered to be a marketing communication. Whilst it is not subject to any prohibition on dealing ahead of the dissemination of investment research we will not seek to take any advantage before providing it to our clients.

Pepperstone doesn’t represent that the material provided here is accurate, current or complete, and therefore shouldn’t be relied upon as such. The information, whether from a third party or not, isn’t to be considered as a recommendation; or an offer to buy or sell; or the solicitation of an offer to buy or sell any security, financial product or instrument; or to participate in any particular trading strategy. It does not take into account readers’ financial situation or investment objectives. We advise any readers of this content to seek their own advice. Without the approval of Pepperstone, reproduction or redistribution of this information isn’t permitted.