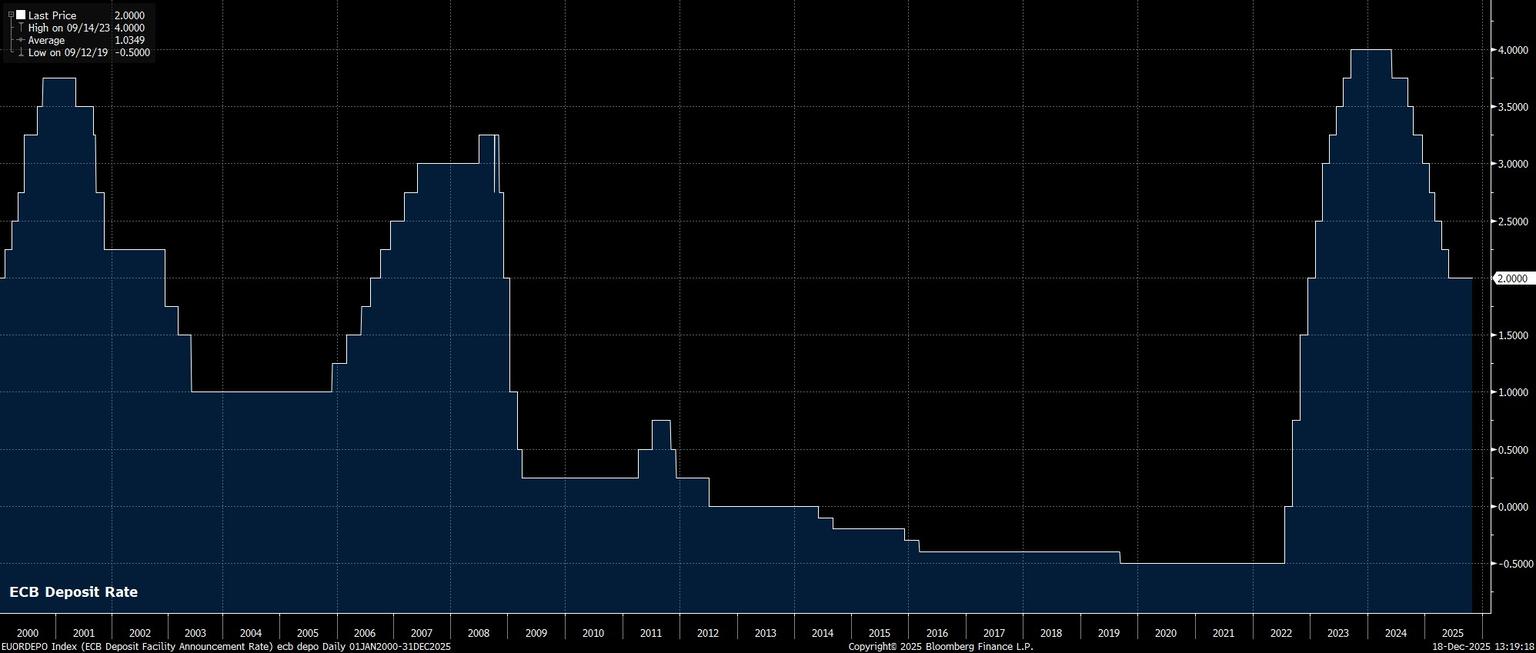

Rates Remain On Hold

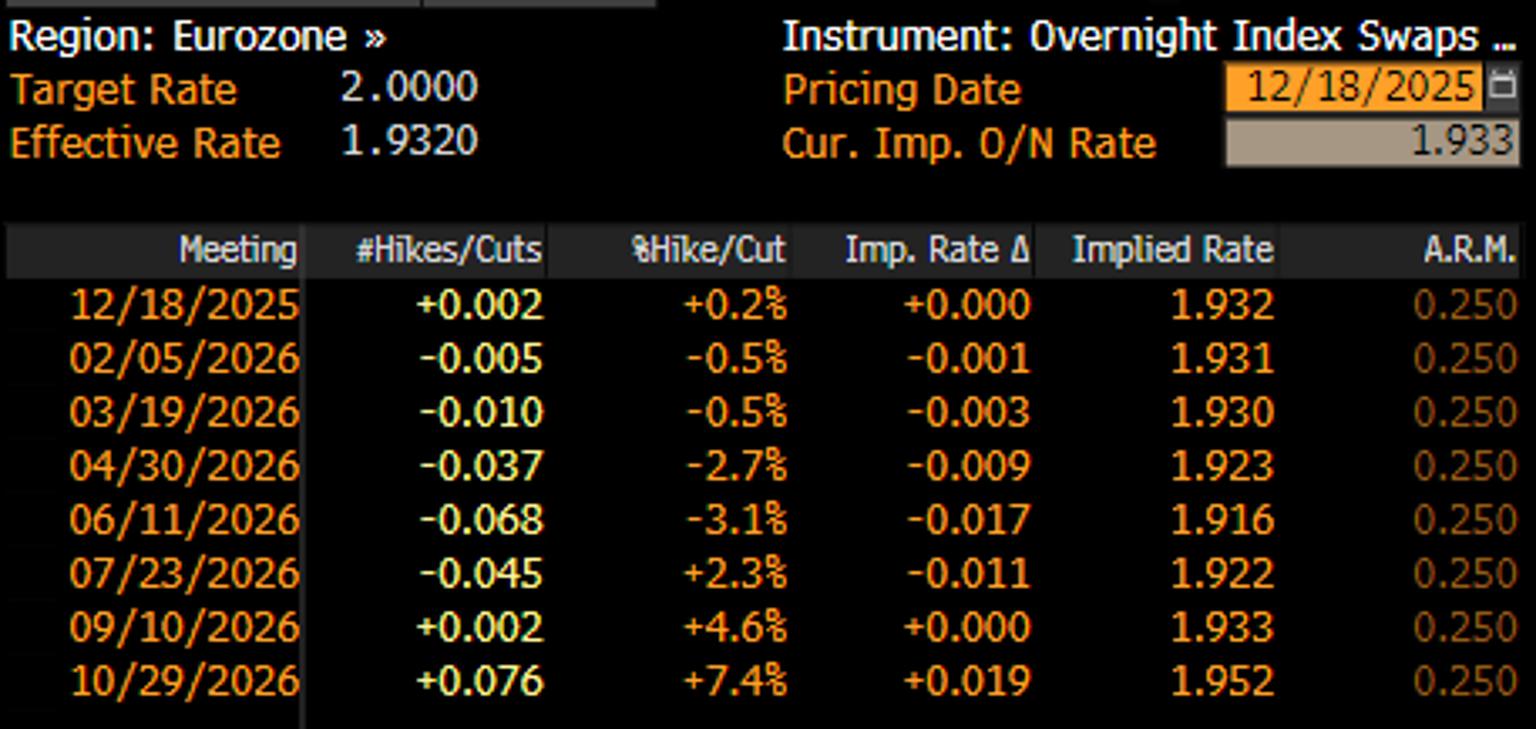

As alluded to, and as had been fully discounted by money markets, the Governing Council held all policy settings steady at this year’s final meeting, with the deposit rate hence being maintained at 2.00%. Such a decision extends the pause that has now been in place since the June confab, and helps to further support the idea that the easing cycle has now come to an end, with 2.00% marking the terminal rate.

Policy Guidance Springs No Surprises

Accompanying the very much expected decision to hold rates steady, was policy guidance that not only came in similarly unsurprising fashion, but with which market participants have now become incredibly familiar.

Consequently, the policy statement reiterated that policymakers will continue to follow a ‘data-dependent’ and ‘meeting-by-meeting’ approach in determining the appropriate policy stance, while again stressing that no ‘pre-commitment’ is being made to any particular pre-set policy path.

Forecasts In Focus

Of considerably more interest than the statement, were the accompanying staff macroeconomic projections.

On growth, the latest projections saw expectations revised higher throughout the forecast horizon, with the ECB staff now pencilling in growth of 1.2% in 2026, followed by growth of 1.4% - roughly potential – in both 2027 and 2028.

Meanwhile, in terms of the inflation outlook, there was a modest upwards revision to the 2026 projection, which now stands at 1.9%, followed by a small inflation undershoot in 2027, before headline inflation returns to the 2% target at the end of the forecast horizon in 2028.

Lagarde Provides Little New Information

Reflecting on the above, at the post-meeting press conference, President Lagarde repeated that policymakers will continue to follow a ‘data-dependent’ and ‘meeting-by-meeting’ approach, while also repeating that the ECB remain in a ‘good place’. Lagarde also confirmed that, unsurprisingly, the decision to stand pat at the final meeting of the year was a unanimous one.

Conclusion

Very much in line with expectations, the Governing Council did nothing to materially alter the policy outlook at the final meeting of 2025, with the deposit rate having been reduced by 200bp from last year’s peak, and now sitting well within the ECB’s range of estimates as to where the eurozone’s neutral rate lies.

Consequently, although some of the GC’s more dovish members may seek to argue the need for further policy accommodation early next year, it remains likely that said policymakers remain in the minority, barring a material deterioration in economic growth, with most rate-setters preferring to focus on incoming ‘hard’ data, as opposed to potentially over-reacting to staff macroeconomic projections.

The base case, then, remains that the ECB’s easing cycle has now come to an end, and that the next rate move – eventually – will be a hike. Such a hike, however, seems highly unlikely to come in 2026, through which the GC are set to stand pat, before addressing the issue of if, and indeed when, to tighten policy towards the second half of 2027.