Consolidation, ETF Outflows & Liquidation Risk – Which Way Will BTC Break?

They say never short a dull market, and while crypto is rarely dull, Bitcoin has certainly entered a period of compression.

Since 6 February, Bitcoin has traded in a tight range, with price capped near $71,500 and supported around $65,270. The bulls have failed to push higher, yet the bears have been equally unable to force a decisive breakdown.

The result is a volatility squeeze that typically precedes a significant move.

For traders and institutional investors alike, the key question now is simple. Is Bitcoin preparing for a breakout, and if so, in which direction?

Market Summary

• BTC trading range: $65,270 to $71,500

• 10-day realised volatility: Now at 20%, below the 12-month average of 35%

• $5.29 billion net exchange outflows in the last 30 days • $3.06 billion year-to-date outflows from spot Bitcoin ETFs

• Fear and Greed Index: 14, signalling extreme fear

• 57% of circulating BTC currently in profit

Volatility Compression Is Building Pressure

Bitcoin’s 10-day realised volatility has fallen to 20%, well below the 12-month average of 35%.

For institutional portfolios, Bitcoin’s volatility is often a feature rather than a flaw. It adds diversification and variance within multi-asset allocations. However, volatility that is too extreme becomes unmanageable, while volatility that is too low reduces tactical opportunity.

At 20%, BTC volatility is arguably near the lower bound of what institutions find attractive. Historically, such compression phases rarely persist. Volatility tends to mean revert, and when it expands, price typically follows.

For now, range trading dominates. Markets do not stay compressed indefinitely.

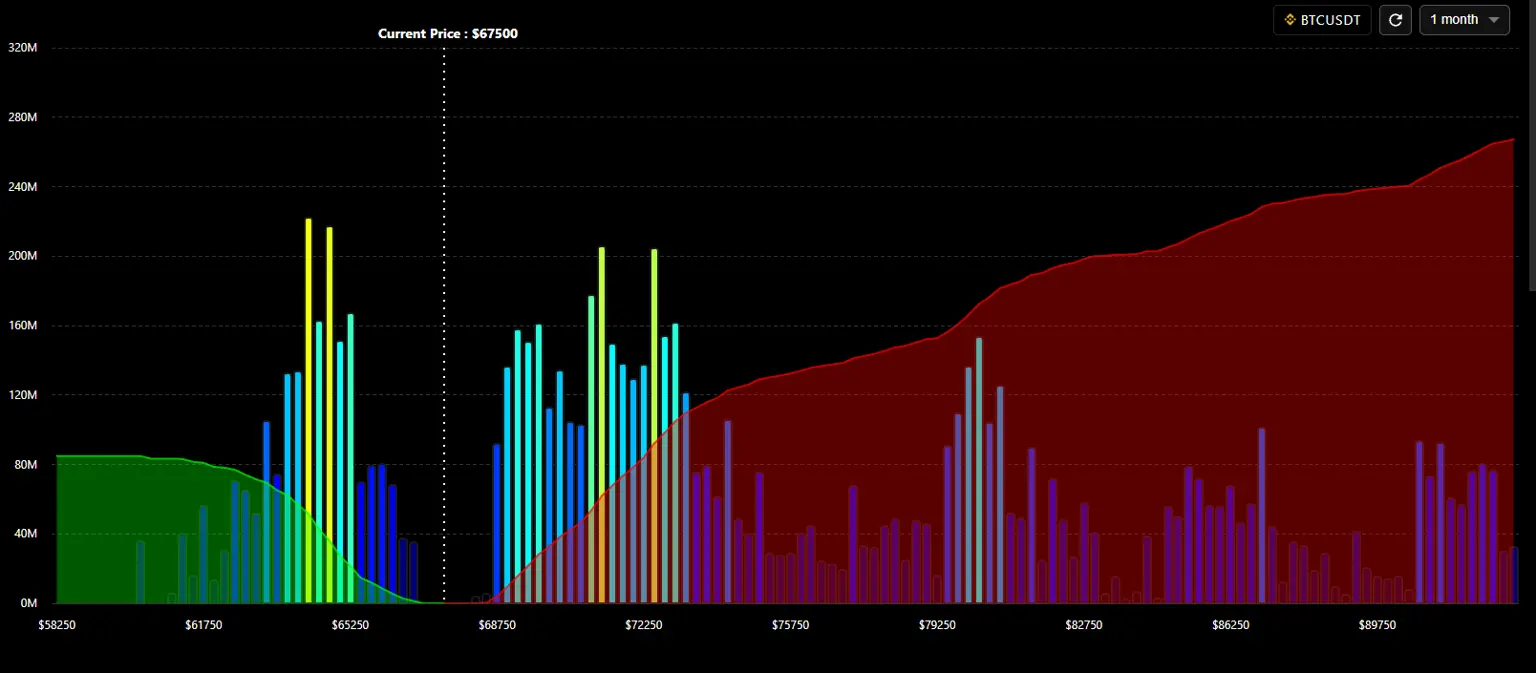

Liquidation Heat Map Points to Possible Upside Risk

The leveraged positioning (chart source: CounterFow) landscape shows a clear skew.

If BTC breaks above $73,000, approximately $122 million in short leverage positions could be forced to liquidate. That cascade could drive price rapidly toward:

• $76,000

• Potentially even $79,000

Liquidation-driven momentum is a defining characteristic of Bitcoin rallies. When upside breaks occur in compressed volatility environments, price persistence can be aggressive.

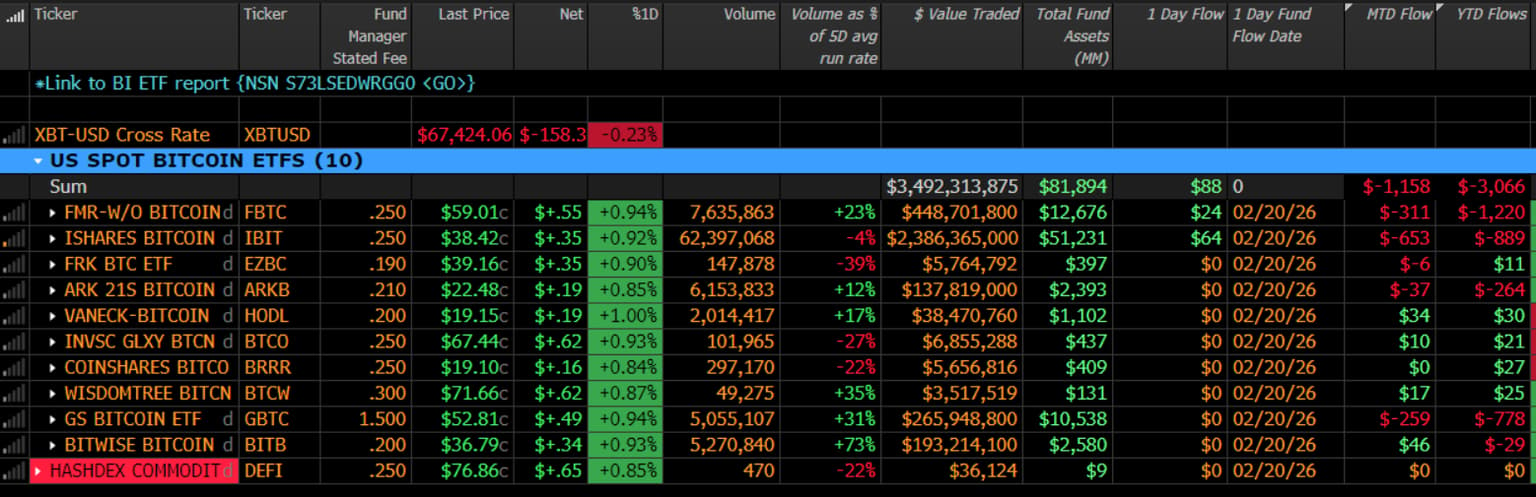

ETF and Exchange Outflows Reflect Weak Sentiment

In the past 30 days, there have been $5.29 billion in net outflows from crypto exchanges, equivalent to roughly 0.4% of total Bitcoin supply. While not systemically large, it reflects cautious positioning.

Spot Bitcoin ETFs have also seen pressure:

• $3.06 billion in year-to-date net outflows

• $1.22 billion of that from the iShares Bitcoin ETF

Volume remains steady but subdued, with approximately $62 million traded over the past five sessions in the iShares product. These flows align with current price action. Consolidation and reduced conviction remain the dominant theme.

Derivatives Activity and Miner Participation Decline

Open interest in Bitcoin derivatives has dropped to its lowest level since November 2024.

There is also limited participation in:

• Bitcoin treasury entities

• Strategy continues to find sellers on rallies.

Extreme Fear Could Become Opportunity

The Bitcoin Fear and Greed Index sits at 14, signalling extreme fear.

Some 57% of circulating Bitcoin remains in profit, the lowest level since January 2023.

Historically, Bitcoin tends to bottom during periods of extreme pessimism and rally when positioning is light. However, sentiment alone does not trigger reversals. Momentum does.

Bitcoin remains a momentum-driven trading vehicle. When price reclaims higher levels and liquidation flows amplify upside movement, that is when conviction typically returns.

CME Introduces 24/7 Bitcoin Futures Trading

One constructive structural development is that CME Group has transitioned Bitcoin futures trading to a 24/7 model. This improves institutional access and price discovery, aligning traditional derivatives markets more closely with crypto’s round-the-clock structure. While it does not directly move price, it enhances ecosystem maturity.

Technical Outlook: Range Now, Expansion Next

Current structure:

• Resistance near $71,500

• Support near $65,270

• Trigger zone for a squeeze above $73,000

Statistically, markets often break in the direction of the prevailing trend, which has been lower. However, that downtrend is now mature, increasing the probability of a counter-trend reversal.

For now, range trading strategies dominate. Traders should remain alert. Compression, extreme fear and declining open interest create conditions that are ripe for expansion.

Final Thoughts

Bitcoin, as is the case in many of the alts, is coiled. Volatility is compressed. Sentiment is washed out. Institutional flows are subdued. Liquidation potential is skewed higher. Markets rarely stay quiet for long.

Whether the breakout resolves lower in line with the primary trend or higher via a short squeeze, the next decisive move is likely to be persistent.

Good luck to all.