- English

- 中文版

Australia Inflation Update: January CPI at 3.8% Consistent with RBA Hiking Rates in May

Summary

- January headline CPI rose 3.8% year-on-year, modestly above expectations.

- Interest rate markets fully price a 25-basis point rate hike from the RBA in May.

- The Australian dollar remains the top-performing G10 currency, supported by relative interest rate differentials.

January CPI Print Keeps Inflation in Focus

Australia may not have a structural inflation crisis, but inflation remains above the preferred range of the Reserve Bank of Australia and continues to show signs of persistence.

The January monthly CPI print showed headline inflation rising 3.8% year-on-year. The trimmed mean measure, closely watched by the RBA as a gauge of underlying price pressures, printed at 3.4% year-on-year.

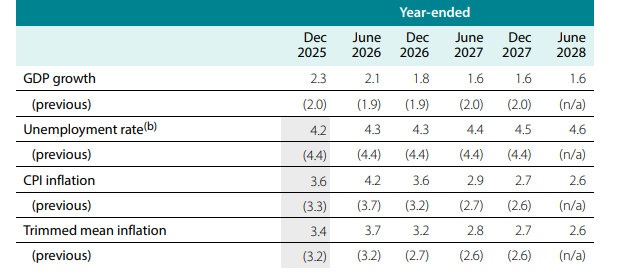

While the result was slightly firmer than market expectations, it broadly aligns with the RBA’s February Statement on Monetary Policy, where headline inflation was forecast to lift toward 4.2% in the June quarter.

The key takeaway is clear: inflation remains sticky enough to justify further modest tightening of rates policy.

What the RBA Is Watching Next

Several key data points will influence the RBA’s near-term policy decisions:

- Q4 GDP: Expected around 2.1% annualised, slightly above the RBA’s estimated potential growth rate of 2%.

- Employment data (19 March): Labour market resilience remains central to policy calibration.

- February monthly CPI (25 March).

- Q1 quarterly CPI (29 April): The most critical release for rate decisions.

Despite the growing importance of monthly inflation data, the RBA continues to place greater emphasis on the quarterly CPI report when assessing policy adjustments.

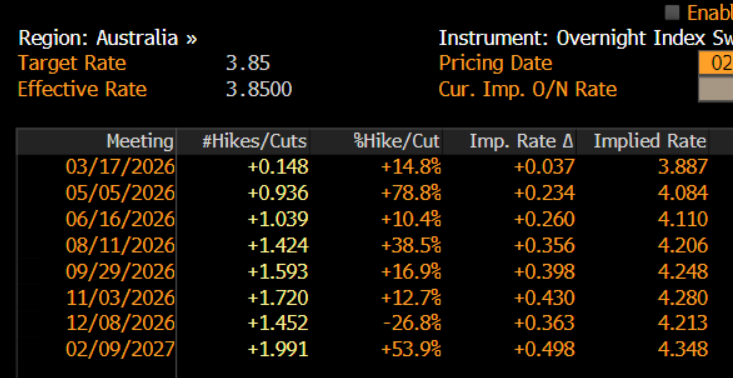

Interest Rate Markets Fully Price May Hike

Interest rate swaps suggest: A modest probability of a rate hike at the March meeting. A fully priced 25-basis point hike at the May meeting. By year-end, one hike is priced with around a 50% chance of a second move. If delivered, this would lift the cash rate toward 4.25%, broadly in line with policy settings seen in late 2023 and 2024. This signals a controlled and measured tightening path rather than the start of an aggressive hiking cycle.

Australian Dollar Benefits from Relative Rate Differentials

The Australian dollar continues to outperform its G10 peers, largely driven by relative rate expectations. While global risk sentiment, trends in Chinese markets, financial conditions, and terms of trade all matter, interest rate differentials are currently providing meaningful support.

- AUD/USD is trading above 0.7100 and eyeing recent highs near 0.7147 - a break here takes the pair to the best levels since 2023.

- AUD/CAD has broken to new cycle highs above 0.9700.

- AUD/NZD prints a higher high, and remains in a strong underlying bull trend. The cross rate eyes a test of 1.1900 and the best levels since 2013.

- GBP/AUD hits new cycle lows, and eyes a break of of 1.9000.

Year-to-date, the Australian dollar has gained 6.5% against the US dollar, making it the strongest-performing G10 currency.

Outlook: Data Dependent but Bias to Tighten

The January CPI print reinforces the case for a May rate hike. However, this remains a data-dependent path rather than a commitment to an extended tightening cycle.

Should upcoming GDP, employment, and quarterly CPI data confirm persistent inflation pressures, markets may begin to price a higher probability of two hikes in 2026.

For now, the balance of risks supports a stronger Australian dollar and a steady, measured tightening bias from the RBA.

The material provided here has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such is considered to be a marketing communication. Whilst it is not subject to any prohibition on dealing ahead of the dissemination of investment research we will not seek to take any advantage before providing it to our clients.

Pepperstone doesn’t represent that the material provided here is accurate, current or complete, and therefore shouldn’t be relied upon as such. The information, whether from a third party or not, isn’t to be considered as a recommendation; or an offer to buy or sell; or the solicitation of an offer to buy or sell any security, financial product or instrument; or to participate in any particular trading strategy. It does not take into account readers’ financial situation or investment objectives. We advise any readers of this content to seek their own advice. Without the approval of Pepperstone, reproduction or redistribution of this information isn’t permitted.