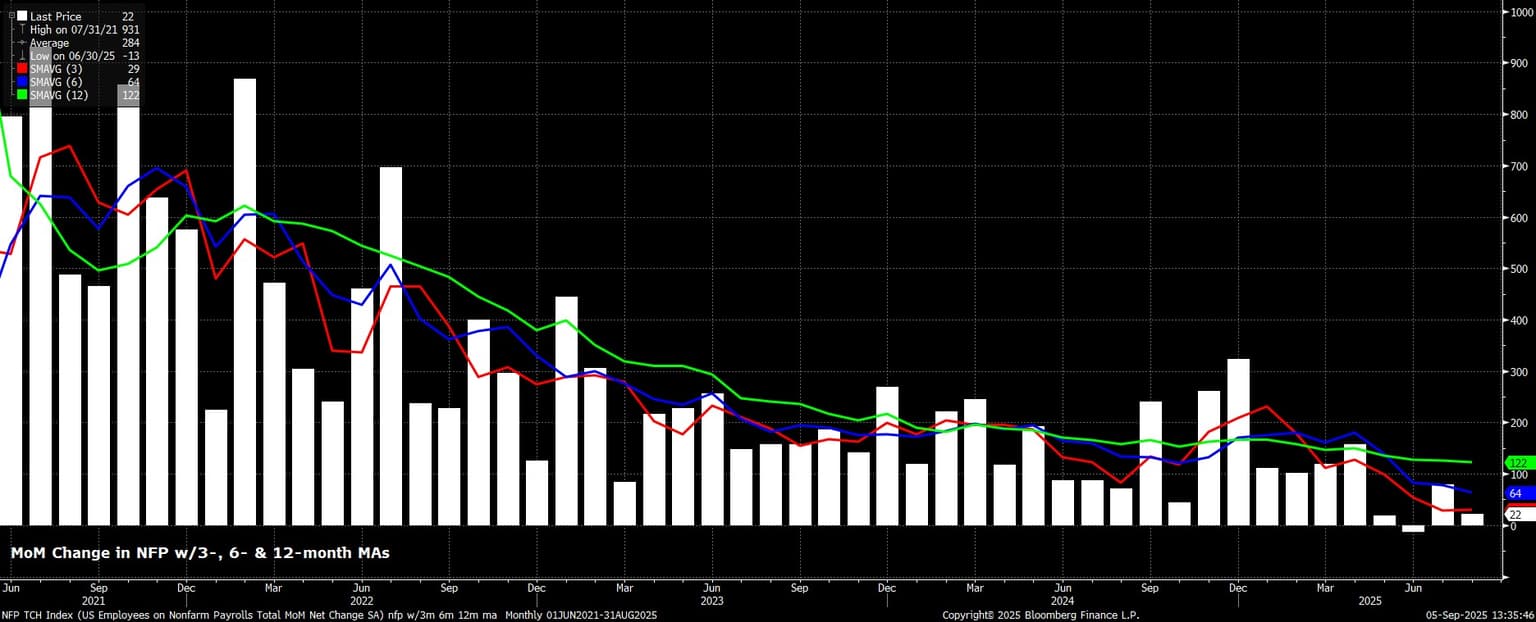

Headline nonfarm payrolls rose +22k last month, considerably below consensus expectations for a +75k increase, but within the typically wide forecast range of 0k to +115k. Concurrently, the prior two payrolls prints were revised by a net -21k, in turn taking the 3-month average of job gains to a rather dismal +29k, probably around half the breakeven pace.

Taking a look under the surface of the payrolls print, things look rather glum. A majority of sectors saw employment decline in August, with those job losses led by Professional & Business Services, and Government employment. Once more, Healthcare (+46k) was the notable growth sector, and continues to prop up the headline figure at large.

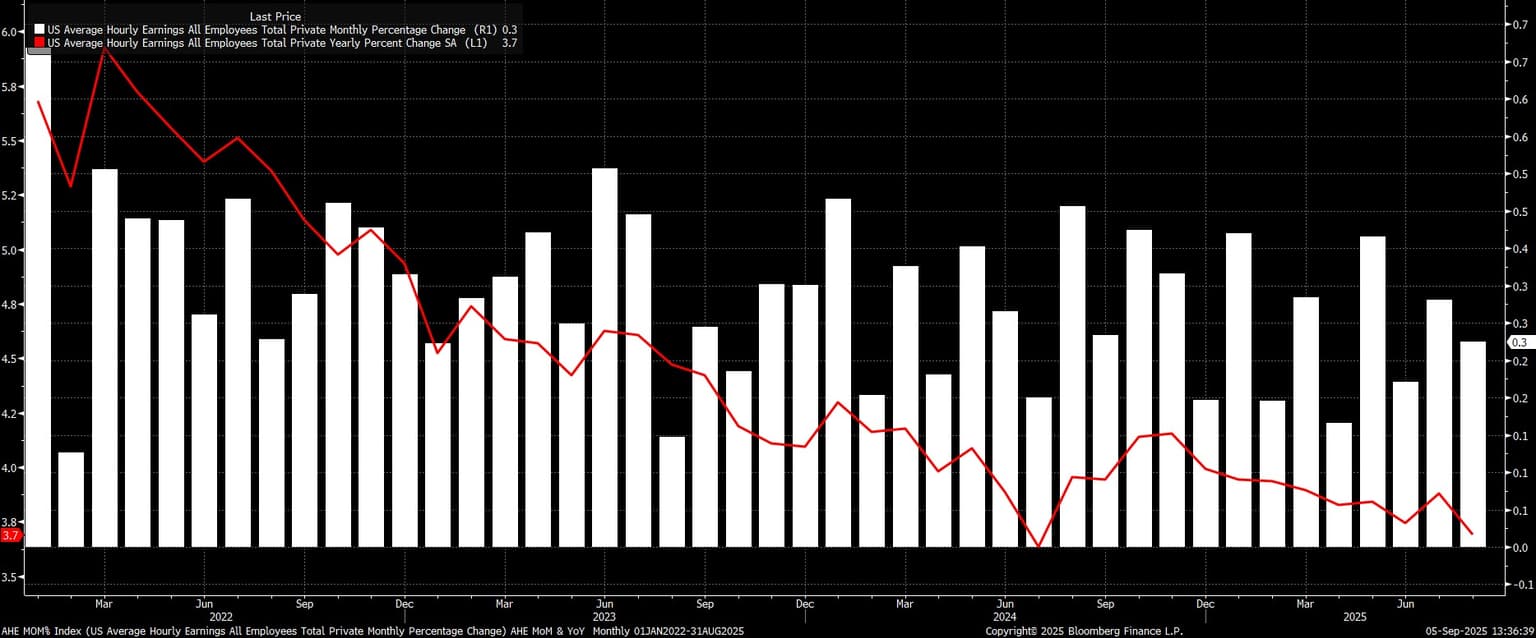

Staying with the establishment survey, the jobs report pointed to earnings pressures again remaining well-contained, reinforcing the FOMC’s long-standing view that the labour market is not a source of significant upside inflation risks at the current time.

Average hourly earnings rose 0.3% MoM, bang in line with expectations, which in turn saw the annual rate cool to 3.7% YoY.

Turning to the household survey, headline unemployment rose to 4.3% last month, in line with expectations, and to a fresh cycle high. This, however, was accompanied by an unexpected rise in labour force participation, to 62.3%.

As has now been the case for some time, though, some degree of caution is still required in interpreting this data, as the BLS continue to grapple not only with a sharp decline in survey response rates, but also amid the rapidly changing composition of the labour force.

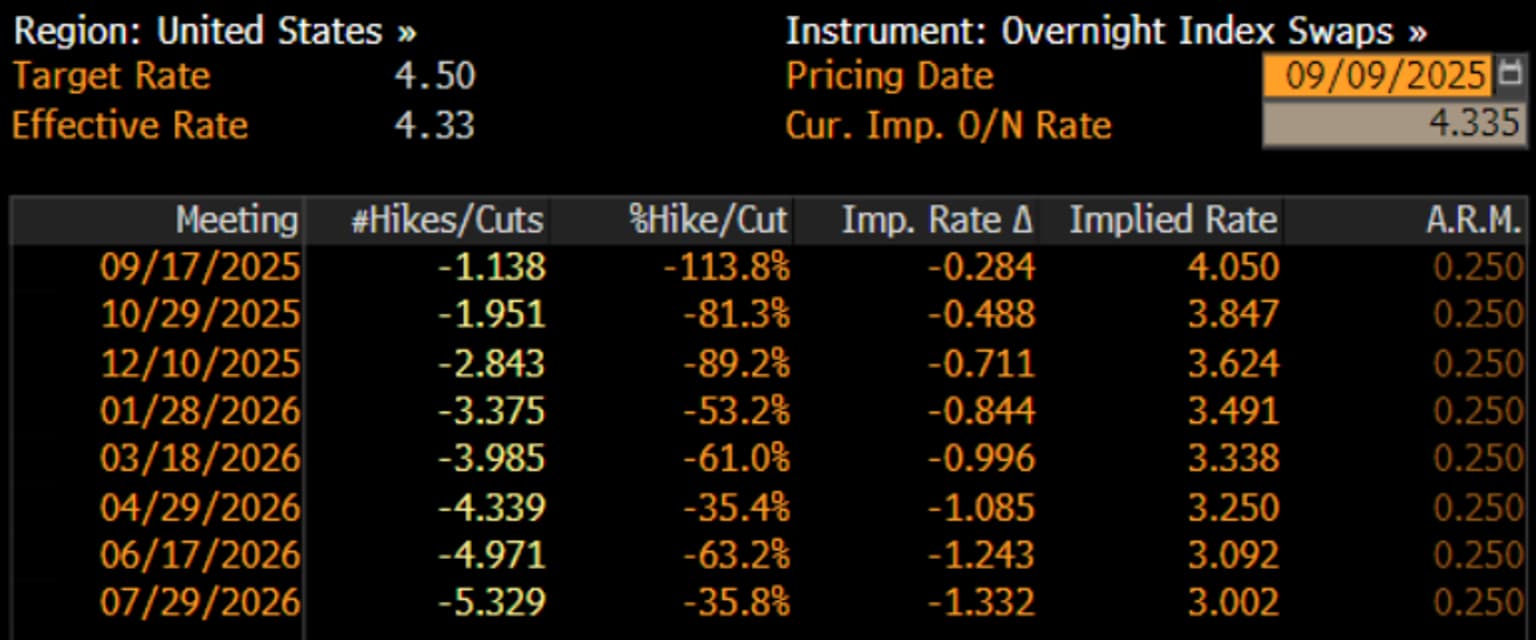

In reaction to the jobs report, market participants continue to fully price a 25bp cut in September, while also now pricing around 66bp of easing by year-end, up from 59bp pre-release, and implying around a 2-in-3 chance of three cuts being delivered this year.

Stepping back, the August jobs report does not materially alter the near-term FOMC policy outlook, and confirms that the labour market continues to lose momentum.

After Chair Powell’s dovish pivot at Jackson Hole, a 25bp cut at the September meeting remains locked-in, as the FOMC look set to take out ‘insurance’ against a loss of momentum in the labour market. While there are likely to be some dissenters in favour of a larger rate reduction, such a move shan’t command support from a majority of Committee members, given continued concern over upside inflation risks, and the desire to ensure that inflation expectations remain well-anchored.

Looking ahead, while the September ‘dot plot’ may give a clearer steer on the likely pace of easing through year-end, my base case is that the September cut will be followed with another such move at the December meeting. Risks to this view, though, arguably tilt marginally in a dovish direction, were material labour market weakness to emerge, though the bar to more aggressive easing is clearly a high one, with headline inflation having been north of target for four-and-a-half years, and being set to accelerate further over the next six months or so.

.png?format=pjpg&auto=webp&width=1536&quality=75&branch=main)