- English

- 中文版

ASX 200 Breaks to New All-Time High of 9,197 as Earnings and Tech Support the Rally

ASX 200 Reaches a Fresh Record High

The ASX 200 has surged to a new all-time high of 9,197, surpassing the previous peak of 9,118 set on 19 February. While intraday price action has been volatile, gains are holding into the latter stages of the session, a constructive sign for bulls at these elevated levels.

A close above 9,200 would have been ideal for momentum traders, but that may require a supportive lead from US markets. For now, the index remains firmly bid, with 64 percent of ASX 200 stocks trading in positive territory.

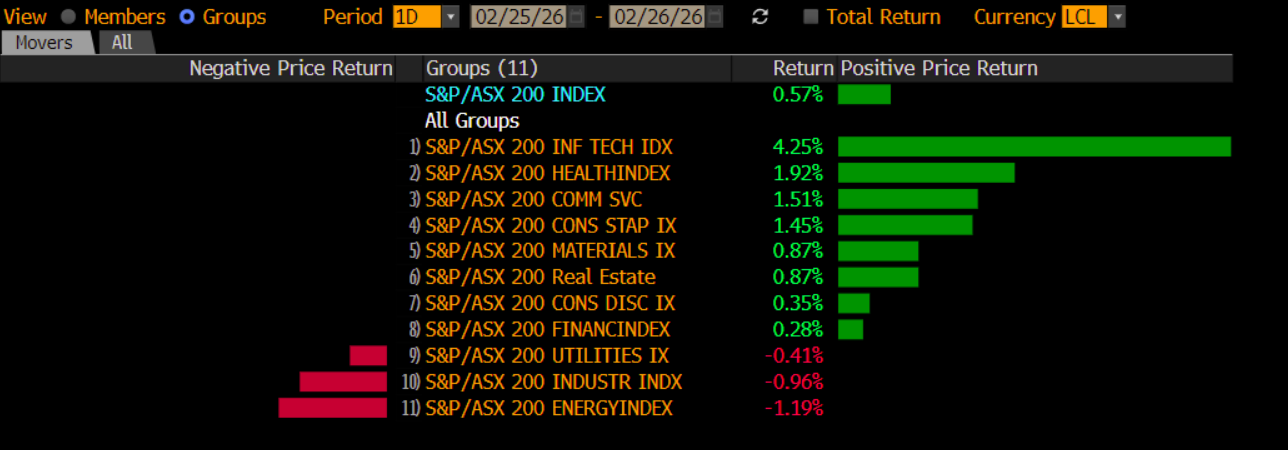

Technology Leads as Short Covering Emerges

Technology stocks have led the gains, recovering after a period of underperformance earlier in the year. Given the prior weakness, there appears to be an element of short covering contributing to today’s upside move.

Healthcare and communication services stocks are also adding support, while the major banks continue to hold firm and provide index stability.

BHP and Rio Tinto in Focus

BHP remains a key stock to watch. The shares briefly pushed toward an all-time high of 58.29 before momentum eased, with the stock oscillating around 58 for much of the session. Price action suggests underlying demand remains intact on modest pullbacks.

Rio Tinto is also contributing positively to index performance. The daily chart shows constructive technical structure, with traders watching for a decisive daily close above 170. This level has capped rallies twice during February, and a sustained break would reinforce the broader uptrend that has been in place since September.

ASX 200 Banks Provide Crucial Support

Within the banking sector, NAB and Westpac are showing relative strength. Commonwealth Bank, the largest weighting in the ASX 200, appears comfortable consolidating in the 175 to 180 range. For the index to break decisively above 9,200, a sustained move above 180 in CBA would likely provide the necessary catalyst.

Strong Year-to-Date Performance and Earnings Momentum

The ASX 200 is now up 5.3% year to date, with total returns even stronger when dividends are included.

Earnings season has been an upside driver. Approximately 86% of ASX 200 companies have reported first-half results. Of those, 43% beat consensus earnings expectations by an average of 10.6%. The same proportion beat revenue forecasts, with aggregate sales growth for the half up 7.2% and earnings growth running at 14.4%.

Over the past four weeks, consensus earnings per share forecasts have been modestly revised higher. Looking ahead, analysts expect aggregate EPS growth of 15.1 percent for the year ahead and 8.9 percent in 2027. This represents a healthy earnings backdrop for the index.

Dividends and Valuations Remain Supportive

Dividend expectations have also improved, with aggregate ASX dividends projected at 302 per share, representing growth of around 5.2% from the prior year.

At 19.1 times forward earnings, the ASX 200 is certainly not cheap, but valuations are not at levels that typically deter capital inflows. The combination of earnings growth and dividend support continues to underpin sentiment.

Macro Backdrop and Interest Rate Expectations

Domestic cyclicals are benefiting from reasonable economic growth. Upcoming Aus Q4 GDP data is expected to show growth slightly above potential at around 2.1 percent. This suggests steady expansion without the need for an aggressive rate hiking cycle.

Markets currently anticipate the RBA cash rate potentially reaching 4.25% over the next 12 months. These expectations are not creating significant distortions within the ASX 200, and volatility remains contained.

Can the ASX 200 Break 9,200?

The ASX 200 may not generate the explosive headlines seen in the NASDAQ, Nikkei, KOSPI or TAEX, but it continues to trend steadily higher with strong price persistence. If Commonwealth Bank can break above 180, BHP remains supported on pullbacks, and energy and materials continue to contribute, a sustained move above 9,200 could come sooner rather than later.

For now, the index remains in a constructive uptrend, supported by earnings strength, dividend growth and a stable macro environment.

The material provided here has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such is considered to be a marketing communication. Whilst it is not subject to any prohibition on dealing ahead of the dissemination of investment research we will not seek to take any advantage before providing it to our clients.

Pepperstone doesn’t represent that the material provided here is accurate, current or complete, and therefore shouldn’t be relied upon as such. The information, whether from a third party or not, isn’t to be considered as a recommendation; or an offer to buy or sell; or the solicitation of an offer to buy or sell any security, financial product or instrument; or to participate in any particular trading strategy. It does not take into account readers’ financial situation or investment objectives. We advise any readers of this content to seek their own advice. Without the approval of Pepperstone, reproduction or redistribution of this information isn’t permitted.