- English

- 中文版

Analysis

There are still many unknowns that traders want answers for, but it does feel like the market has looked at the US and EU banking landscape and formed a more constructive view.

After the UBS/Credit Suisse merger, EU banks have become less of a concern and the market's spotlight is firmly on the US regional banks. It’s here where we continue to see significant bank deposit outflows, specifically out of the smaller/regional banks with migration into larger financial institutions and money market funds.

We also see massive demand from the smaller/regional banks for loans through the Fed’s weekly credit facilities. Until this demand abates, and we see far less take-up of these loans then US regional banks – and by extension bond and equity indices CFDs markets - will remain volatile.

Watching high yield credit spreads

The market is seeing fragility in the US commercial real estate market, notably in the office space. Importantly, this looks contained and at this stage it’s not flowing through to a genuinely worrying blowout in high-yield (HY) corporate credit spreads. We saw HY corporate credit deteriorate by some 100bp into 5.16%, through mid-March, but until this pushes well past 6%, I think broad markets will lack any real fear.

Through 6% is where a wider range of US corporates will have to pay up for funding when they need to raise or rollover maturing debt.

The HYG ETF (iShares high yield corporate ETF) is a good vehicle to see/trade the riskier part of credit markets, and it is one of the most important markets for all macro-focused traders. It’s here that if we see the HYG smash below $70 (and the Oct lows) that we’d likely see the US500 really crater, the JPY rally, and the VIX index above 35%.

Interest rate expectations well correlated to bank equity

The market has been expressing the ebb and flow of bank instability risk through the interest rate futures. US bank equity trades lower, notably in the KBE ETF (S&P regional bank ETF) and the market buys fed funds and SOFR futures, increasing rate cut expectations.

The second-order effect was a rally in gold and Bitcoin rally, while we saw traders targeting growth sectors in equity, with mega-cap tech a noticeable performer.

Few will forget the recent moves in interest rate expectations, where the turn in pricing was wild – from 9 March to 15 March the market moved from pricing 30bp of hikes (between May ‘23 to December ‘23) to 126bp of cuts.

The message this sent was that the banks were going to cause an imminent recession in the US.

However, after the initial panic, we see the degree of cuts priced through this period falling hard from 126bp to currently 54bp (traders can see this on TradingView using this code: ((100-CBOT:ZQZ2023)-(100-CBOT:ZQK2023)), with the futures curve seeing the Sept FOMC meeting as the most likely stage for the Fed to start cutting, with an acceleration seen into 2024.

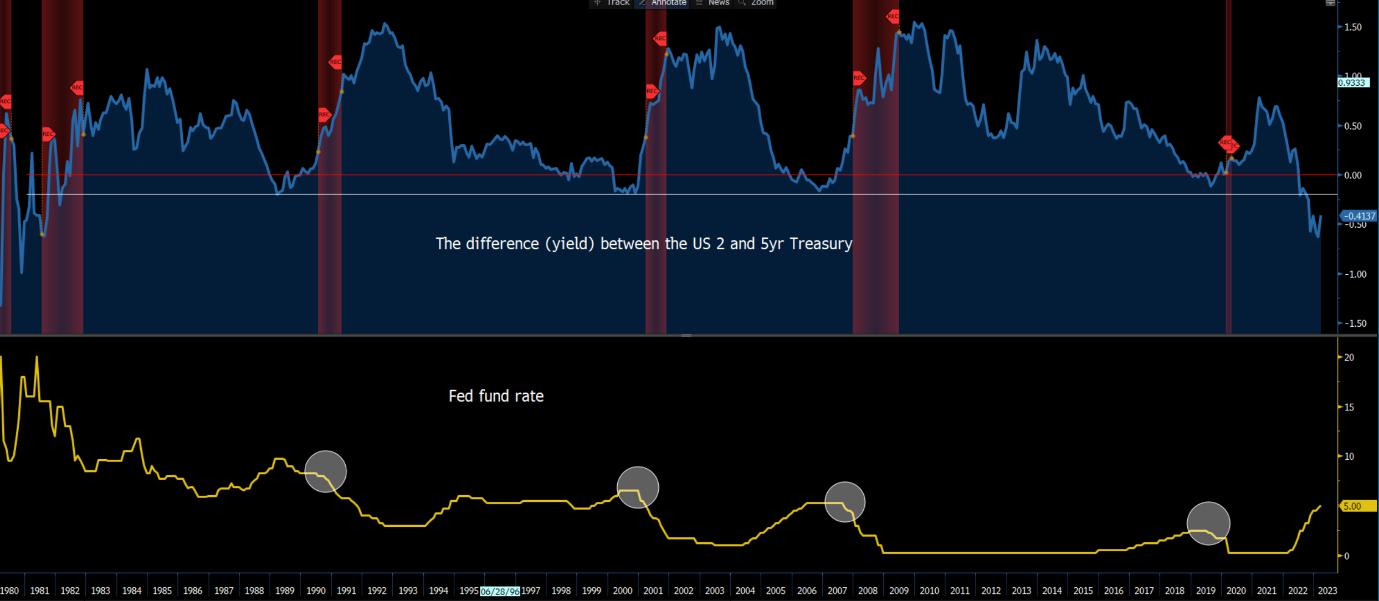

Watching the US Treasury yield curve

The moves in rate expectations manifested in a steeper US Treasury yield curve. We’ve seen the difference (in yield) between the US 2-year and 30yr Treasury rising from -120bp to 0. The 2-year vs 5-year Treasury curve (traders can see this on TradingView using this code TVC:US05Y-TVC:US02Y) has risen from -72bp to sit at -41bp.

This is classic late economic cycle type activity and as we’ve seen since the 1980s, it’s when the curve heads from inversion back into positive territory, as 2yr yields fall faster than the longer maturities, that the Fed cut rates.

Typically, in this environment we see the USD trend lower – notably USDJPY - and gold finding form. Long NAS100 / short US30 would work well in this environment. So, the 2’s 5s US treasury curve is firmly on the macro watchlist.

The KRE ETF is front and centre

HY credit and yield curves aside, it's US bank equity that is central to everything – a leg lower in the KRE ETF through $40 would likely come with renewed rate cuts being priced and traders buying tech and gold. Conversely, a rally through $50 would see cuts further priced out of the market and short NAS100 / long US2000 working well as a trade.

Considering as US bank's cost of capital is on the rise, the pace of loan growth is falling hard and there are still rising concerns on commercial real estate, having conviction on bank share price appreciation is limited.

Another key consideration is around the supply of credit into the real economy. We’ve seen banks’ lending standards rising rapidly since July 2021, and it is becoming ever tougher for a business to get a loan. On the current trajectory, the Fed’s well-watched senior loan officer survey (will be known the Fed for May FOMC meeting) on bank lending practices is on course to test the extreme highs we saw in 2020.

Banks are being more and more selective when lending and this dynamic is typically associated with increased recession risk – we see it also closely correlated with high-yield credit spreads, and drawdown in the US500.

So, US banks remain front and centre – I am sceptical we get 50bp of cuts this year unless we see another leg lower in bank equity, weekly jobless claims rise, and core inflation pulls back. However, there is much to play for and real risks in the system that could suggest the Fed may have to ease. I am watching the yield curve, credit markets and banks (specifically the KRE ETF) as my central guide - it does feel like we’re in for a big Q2 in global markets.

The material provided here has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such is considered to be a marketing communication. Whilst it is not subject to any prohibition on dealing ahead of the dissemination of investment research we will not seek to take any advantage before providing it to our clients.

Pepperstone doesn’t represent that the material provided here is accurate, current or complete, and therefore shouldn’t be relied upon as such. The information, whether from a third party or not, isn’t to be considered as a recommendation; or an offer to buy or sell; or the solicitation of an offer to buy or sell any security, financial product or instrument; or to participate in any particular trading strategy. It does not take into account readers’ financial situation or investment objectives. We advise any readers of this content to seek their own advice. Without the approval of Pepperstone, reproduction or redistribution of this information isn’t permitted.