- English

- 中文版

2 Out Of 2 Upside Inflation Surprises – Will CPI Be A Third?

Firstly, on Monday, the latest survey of consumer expectations from the New York Fed pointed to a noticeable uptick in both short-, and longer-run metrics:

- 1y: 3.3% vs. 3.0% prior

- 3y 2.8% vs. 2.9% prior

- 5y: 2.8% vs. 2.6% prior

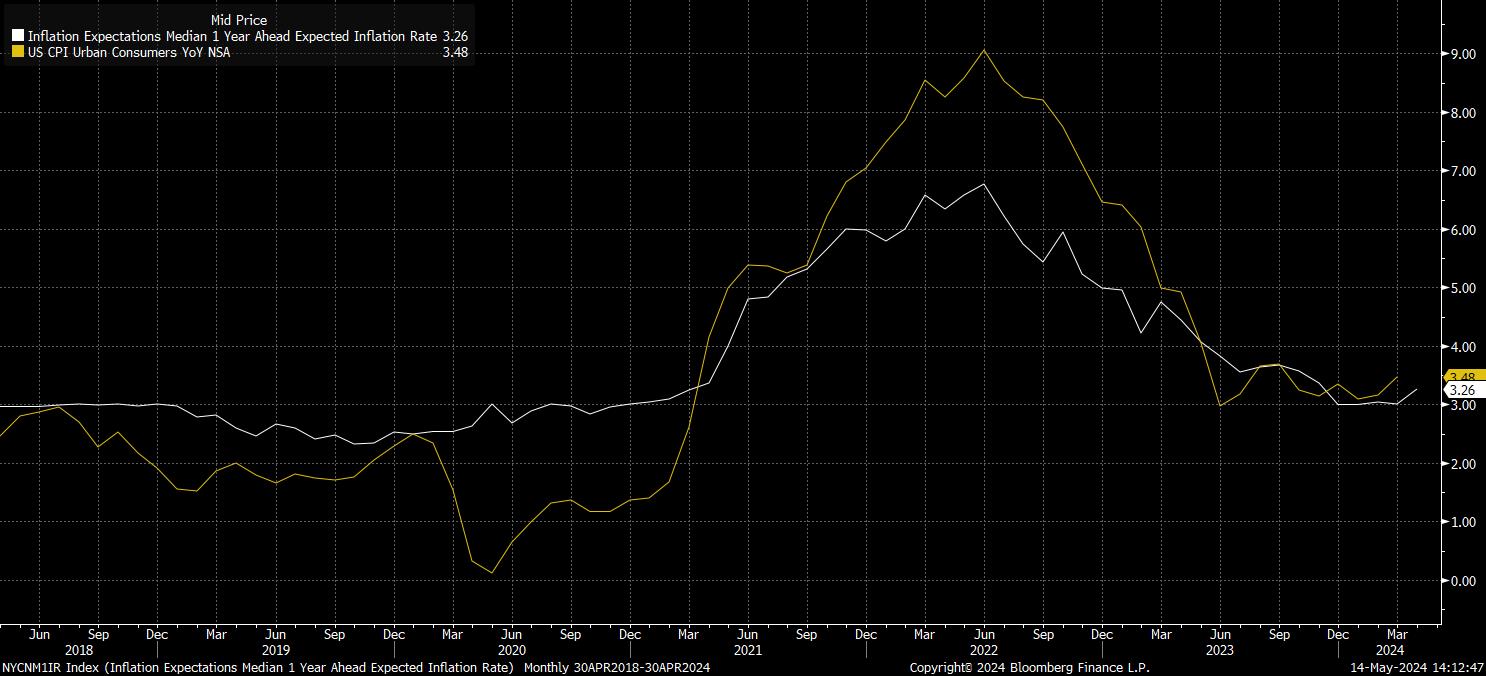

While this did elicit a modest hawkish reaction, most evidently in the front-end of the Treasury curve, there is a slight issue – consumers have an abysmal track record at predicting inflation. Shifts in inflation expectations are typically closely tied to moves in actual inflation, as opposed to the general public looking into their proverbial crystal balls to judge where inflation may end up, as the chart shows.

Secondly, PPI, which came in hotter across the board. Both headline and core PPI rose 0.5% MoM in April, while also rising by 2.2% YoY and 2.4% YoY respectively, with the annual metrics also coming in somewhat hotter than consensus had expected.

At face value, a worrying report. However, there is again something of a problem with such a top-level assessment. Digging into the data, one notices that the MoM prints were revised sharply lower in March, by 0.3pp to -0.1% MoM apiece. Hence, effectively, the 0.3pp beat vs. consensus in the April data, nets off against the downward revision to the prior month’s figures, helping to explain the short-lived nature of the hawkish cross-asset reaction seen in the aftermath of the print crossing newswires.

So, where does this leave us ahead of CPI tomorrow?

In short, I’d argue that both of the above represent more ‘noise’ than they do ‘signal’, particularly when the statistical relationship between a PPI beat and subsequent upside CPI surprise is, at best, ropey. Instead, risks to the April CPI figure appear to be relatively evenly balanced. While energy prices, driven primarily by gasoline, continued to rise on the month, food inflation was a touch soft, and used car prices also notched a relatively significant decline.

Nonetheless, with the YoY headline CPI metric having surprised to the upside of consensus expectations for three straight months, plenty will be expecting another such beat of the 3.4% median expectation.

Interestingly, the CPI fixings market is priced for a print marginally hotter than consensus on an annual level, at 3.41% YoY, while also pricing a marginally cooler than consensus MoM print, at 0.36% MoM.

Whatever, the short-term playbook over the CPI figure is relatively straightforward. A hotter-than-expected figure will likely elicit a hawkish reaction (stocks & bonds softer, USD firmer), with the magnitude of such a move greater, the greater the degree of surprise.

Naturally, the inverse is true on a cooler than expected figure, though given the aggressively hawkish nature of Fed pricing – per the USD OIS curve – with just 40bp of easing priced through year-end, the balance of risks points to a more significant reaction in the event of a cool print. This is particularly the case with the FOMC having set an incredibly high bar to delivering another hike, while also appearing somewhat desperate to cut rates, particularly in the event of potential labour market weakness.

Related articles

The material provided here has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such is considered to be a marketing communication. Whilst it is not subject to any prohibition on dealing ahead of the dissemination of investment research we will not seek to take any advantage before providing it to our clients.

Pepperstone doesn’t represent that the material provided here is accurate, current or complete, and therefore shouldn’t be relied upon as such. The information, whether from a third party or not, isn’t to be considered as a recommendation; or an offer to buy or sell; or the solicitation of an offer to buy or sell any security, financial product or instrument; or to participate in any particular trading strategy. It does not take into account readers’ financial situation or investment objectives. We advise any readers of this content to seek their own advice. Without the approval of Pepperstone, reproduction or redistribution of this information isn’t permitted.