- English

- 中文版

Daily Fix: Traders managing exposures ahead of G20 Summit

Take, for example, the barrage of headlines brewing in the lead-up to the G20 meeting, which plays out this Friday and Saturday. The real focus falls on the Trump-Xi meeting, which looks to be taking place 12:30 pm AEST on Saturday. Small focus also falls on the Trump-Putin meeting, which takes place at 3 pm AEST.

Expectations for progress set sufficiently low enough

Over the past 15 hours or so we’ve heard from US Treasury Secretary Steven Mnuchin suggesting (and referring to a US–China trade deal) that they “were about 90% of the way there” and that “there’s a path to complete this.” There were some buying of equities and risk on the back of these headlines, although the market didn’t get overly excited as it was seen in the past tense, with Mnuchin recalled saying they were 90% there in April shortly before Trump slapped fresh tariffs on China on 5 May.

Hu Xijin, the widely followed editor of the Party-owned China Global Times, then responded to Mnuchin’s comments on Twitter, detailing "no Chinese official now speaks with such optimism,” and “with dozens of hours left before Xi-Trump summit, Chinese state media has been keeping criticising the US harshly, a situation that never happened in the previous China–US summits." This doesn’t sound like China is coming to the party with ideas of making a deal.

We also heard from US President Donald Trump himself, stating that: “My plan B is that if we don’t make a deal, I’ll tariff, and maybe not at 25% but maybe at 10%. But I’ll tariff the rest of the US$600bil that we’re talking about. My attitude is I’m very happy either way.” This is expectation management 101. The bar for a clear resolution at this G20 summit is now set accordingly.

The bottom line is the market has been hit by a barrage of noise that gives us less clarity than before.

Indecision seen in market moves

With such conflicting headlines, it’s no real surprise to see US equity indices doing very little. If we also look at the S&P 500 (US500) through the cash session, the tape showed a slow bleed lower. If it weren’t for a 2.7% rally in crude driven by a monster 12.7mil barrel draw in the weekly DoE inventory report, which was over a two-standard-deviation event from the five-year average, then US equity indices would have been far lower on the session. I touch on the setup (see below) in WTI crude in Chart of the Day, as we’ve hit the double-bottom target and horizontal resistance, so it wouldn’t surprise to see consolidation here.

We’ve seen reasonable selling in the US bond market overnight, but let’s not forget the world is very long bonds. After James Bullard comments yesterday (which I covered in yesterday’s note), there’s a slight paring back of expectations for a 50bp cut in the July FOMC meeting. This remains a huge question for markets: Will we see a 50bp or 25bp cut from the Federal Reserve in July’s FOMC meeting?

USDJPY has pushed into 107.70 following the move in US Treasury yields. But it feels like traders are lining up to sell rallies in this pair, though a look across the Asian markets we can see far more optimistic moves, which I’ll touch on in my daily Trading Wrap video.

Keeping the USD firmly on the radar

It’s the USD specifically that’s of interest as we head into and post the G20 summit. It feels as though the market is looking for a sustained move lower.

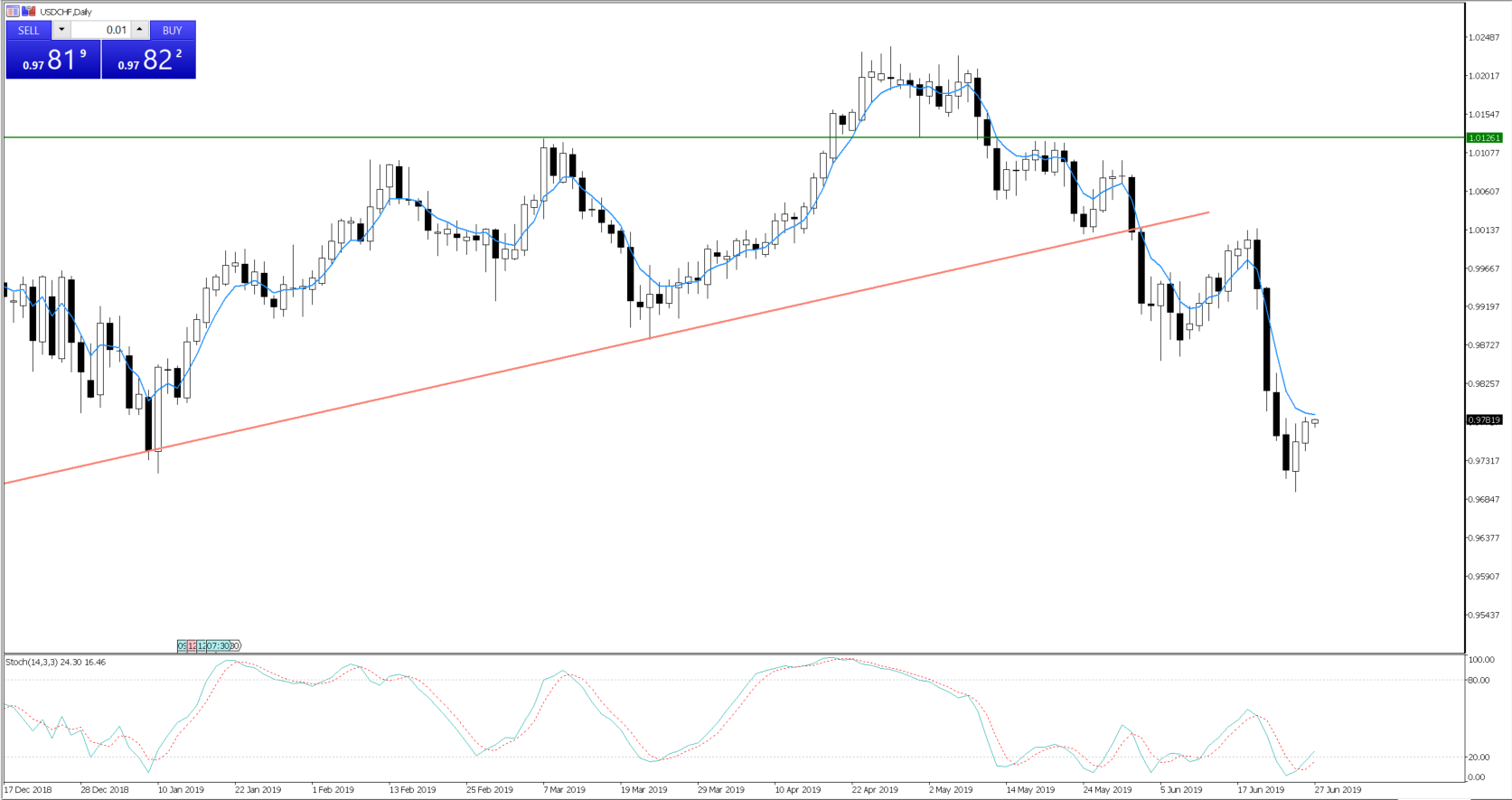

"USDCHF testing the five-day EMA"

Trump seemingly agrees, having again disclosed that the US dollar is too strong and EUR too weak. While I’ve not really heard any scuttlebutt for any bilateral or multilateral agreement to weaken the USD, the outcome of the summit could influence expectations for a 50bp cut from the Fed. We know the central bank is looking at what’s said or not said. While the most likely situation is we simply hear a lot of bravadoes that the two sides plan to work closely together and agree to find an amicable solution, we still need to consider if the event poses a gapping risk for markets. Could we hear something that gives us genuine encouragement, and we see price open significantly from Friday’s close?

It certainly feels as though the probability is we’ll see traders manage exposures, refraining from adding too much additional risk just in case.

So, if the G20 proves to be a non-event, aside from broad financial conditions and inflation expectations, these data points should go some way to answering the 25/50bp debate:

- US ISM manufacturing: 2 July

- US Services ISM: 4 July

- US non-farm payrolls: 5 July

- US CPI: 11 July

The material provided here has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such is considered to be a marketing communication. Whilst it is not subject to any prohibition on dealing ahead of the dissemination of investment research we will not seek to take any advantage before providing it to our clients.

Pepperstone doesn’t represent that the material provided here is accurate, current or complete, and therefore shouldn’t be relied upon as such. The information, whether from a third party or not, isn’t to be considered as a recommendation; or an offer to buy or sell; or the solicitation of an offer to buy or sell any security, financial product or instrument; or to participate in any particular trading strategy. It does not take into account readers’ financial situation or investment objectives. We advise any readers of this content to seek their own advice. Without the approval of Pepperstone, reproduction or redistribution of this information isn’t permitted.