- English

- 中文版

Has the Fed doomed the dollar?

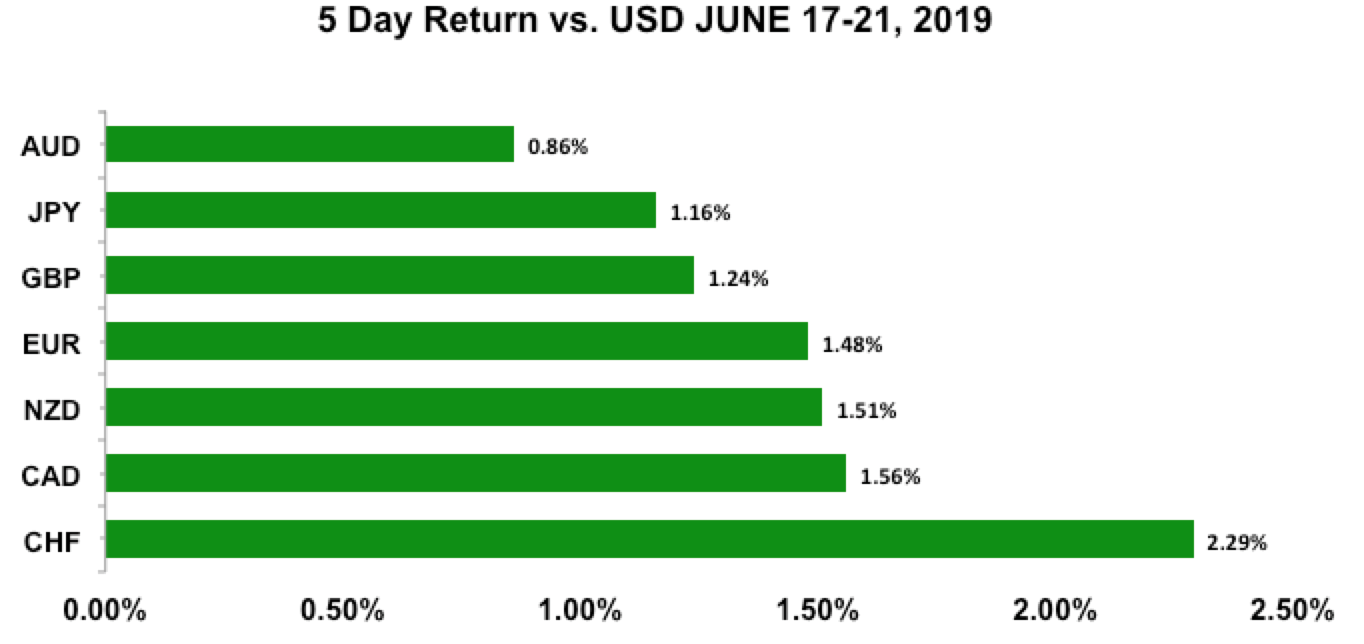

n many ways the Fed has doomed the greenback. But how much it rises or falls will depend on many factor. We got a taste of that in this week’s trade, where the dovish monetary policies of the Reserve Bank of Australia and European Central Bank caused the Aussie and euro to trail behind. In the week ahead, there are very few market-moving economic reports in the US calendar, but there are many major political stories that could ignite big moves in currencies. Most of them centre on the end-of-week G20 summit, but investors should also keep an eye on Iran. US Pres<!--td {border: 1px solid #ccc;}br {mso-data-placement:same-cell;}-->In the week ahead, there are very few market-moving economic reports in the US calendar, but there are many major political stories that could ignite big moves in currencies.ident Donald Trump called off a strike 10 minutes before it was set to happen, but they could come up with another strategy to retaliate to Iran’s shooting of an unmanned drone in international waters. As for the G20, if trade talks between the US and China are rekindled, it’ll lead to a relief rally for USD/JPY.

Weekly trade ideas: Don't miss these market-moving opportunities identified by BK Forex.

US DOLLAR

Data review

- Fed moves closer to cutting rates: Dot plot shows eight members favouring 25bp cut in 2019.

- Empire State survey -8.6 vs 11 expected

- NAHB housing market index 64 vs 67 expected

- Housing starts 1269K vs 1239 expected

- Building permits 1294K vs 1292K expected

- Current account balance -$130bil vs -$124bil expected

- Jobless claims 261K vs 220K expected

- Philadelphia fed survey 0.3 vs 10.4 expected

- Existing home sales vs 5.3mil expected

Data preview

- New home sales: Housing market should be supported by the prospect of no rate cuts this year.

- Consumer confidence index: Lower stocks, rising trade tensions and lower University of Michigan index should hurt confidence.

- Durable goods orders: Big-ticket orders are hard to predict, but stabilization is likely after drop in April.

- Revisions to Q1 GDP: Revisions are hard to predict, but changes can be market-moving.

- Personal income and spending: potential upside surprise given rise in retail sales.

Key levels

- Support 106.50

- Resistance 108.50

US-dollar traders brace for 2019 easing

Thanks to the Fed, the short-term pullback in the US dollar has now turned into a long-term top. There’s widespread support inside the central bank for not one but possibly two interest-rate cuts this year. Considering that the Fed still maintained a hawkish bias in March and a large subset of traders were skeptical of even one 25bp rate cut this year, the possibility of 50bp of easing sent the dollar crashing through support levels. Traders were caught completely off guard as they never expected the Fed to be as dovish as other central banks. Unemployment is low and stocks at record highs, but the Fed could no longer ignore the slowdown in global growth and inflation. At first they felt that the impact would be temporary, but they’re now worried about the broader effect on the economy — so much so that eight members see the need for a rate cut this year, with seven forecasting two cuts. Back in March, no one saw the need for easing.

These changes alone justify a prolonged sell-off in the greenback. But traders need to be selective about the currencies they choose to buy versus the dollar. USD/JPY is the most sensitive to headline risk. If US President Donald Trump and Chinese President Xi Jinping reach a trade deal, we’ll see USD/JPY trade back up to 109. But if the talks fail to take a positive turn, the combination of continued trade tensions and a dovish Fed will allow USD/JPY to slip down to 105. While euro, sterling and Aussie are benefiting from US dollar weakness, they’re the least attractive currencies to buy because their central banks are also actively thinking about easing. Sterling, on the other hand, will be hampered by ongoing Brexit uncertainty. The Canadian dollar and Swiss franc are the most appealing, but the New Zealand dollar could also be attractive if the Reserve Bank suggests that they have no immediate plans for a follow-up move to their rate cut in May.

At the same time, we feel that the market is overly dovish in their expectations for a July rate cut. Fed Chair Powell still had good things to say about the economy, including the labour market, which he described as strong. He downplayed the urgency to ease, and made it clear that they’re in “wait and see” mode. He said that they “expect to learn a lot more about the risks in the near term,” and if data or the risk picture worsens, they have enough support within the central bank to ease quickly. While it won’t take much to push them to action, they’ll still wait for one or two months of disappointing CPI or NFP numbers. The record-breaking moves in stocks buy them time but not for long. All of this means we could see a near-term dollar bounce, particularly given the lack of market-moving US data in this week’s calendar, but the broader trend for the dollar will be lower.

If you missed the Fed meeting, here’re the six main things you need to know about this month’s Fed meeting:

- Fed leaves interest rates unchanged, and drops the word “patient” from policy statement.

- For the first time, dot plot signals interest-rate cut — eight out of 17 members see rate cut this year (seven of those favor two rate cuts).

- Fed is worried that inflation, manufacturing activity, trade and business investment will fall further.

- Fed lowers inflation projections, as well as upgrades GDP and unemployment-rate forecast.

- Job creation and consumer spending won’t be enough to offset downside risks.

- Fed, nonetheless, wants to see more. They expect to learn a lot more from incoming data and risk picture in the near term.

AUD, NZD, CAD

Data review

Australia

- RBA minutes confirm next move in rates is lower.

New Zealand

- PMI services 53.6 vs 52 previous

- Q2 Westpac consumer confidence 103.5 vs 103.8 previous

- Q1 current account balance 0.675bil vs 0.16bil expected

- Q1 GDP QoQ 0.6% vs 0.6% expected

- Q1 GDP YoY 2.5% vs 2.3% expected

Canada

- Manufacturing sales -0.6% vs 0.4% previous

- CPI 0.4% vs 0.1% expected

- CPI YoY 2.4% vs 2.1% expected

- Retail sales 0.1% vs 0.2% expected

- Retail sales ex auto 0.1% vs 0.4% expected

Data preview

Australia

- No major data

New Zealand

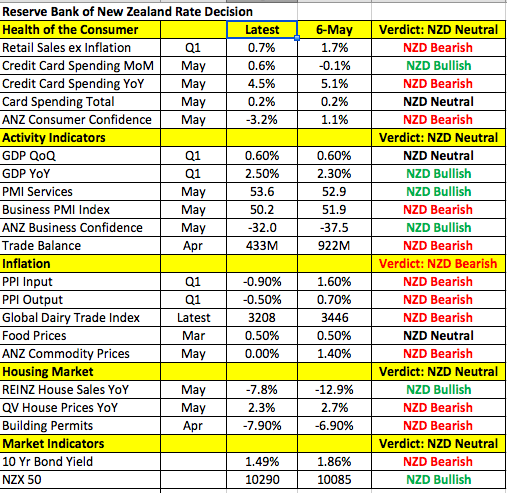

- RBNZ rate decision: no rate cut expected, but RBNZ should keep the door open to easing

- Trade balance: likely to be weaker given sharp deterioration in PMI manufacturing index

- ANZ Business and Consumer Confidence: both likely to be softer given slowdown in Australian and Chinese economies

Canada

- GDP: sharp improvement in trade but retail sales weakened

Key levels

- Support AUD .6900; NZD .6500; CAD 1.3100

- Resistance AUD .7000; NZD .6600; CAD 1.3400

Upside Risk for Aussie dollar

All three of the commodity currencies are benefiting from the sell-off in the US dollar, and we could see a stronger recovery in the Aussie in the coming days. Recent comments by the Trump Administration boosted optimism for cooler trade tensions, which should benefit the Aussie and Kiwi. We won’t know until the weekend if the talks between Presidents Trump and Xi went well, but in the lead-up we expect to see further profit-taking on short AUD/USD positions. There are no major Australian or Chinese economic reports to threaten the rally, so there’s plenty of upside potential for the currency.

The New Zealand dollar, on the other hand, will take its cue from the Reserve Bank’s meeting. Last time, they cut interest rates by 25bp. The decision took NZD/USD to a six-month low, but the drop didn’t last, because the central bank suggested that they were one and done. Since then, we haven’t seen a clear trend in New Zealand’s economy. The latest GDP numbers were strong, and service sector activity is up. Manufacturing activity, inflation and spending are lower, but that may not be enough to convince the RBNZ that another rate cut is needed. There’s no doubt that the global economy is weakening, and it’d be remiss for the RBNZ to not express concerns. But how the New Zealand dollar responds will depend on how aggressive the RBNZ thinks they need to be about easing. If they feel that another preventive rate cut is needed, NZD/USD will reverse its gains quickly but if they leave most of their policy statement unchanged, NZD/USD could hit 67 cents easily in the coming days.

The Canadian dollar should start to underperform. Canada has been one of the strongest economies and, in many ways, still is. But after last week’s disappointing retail sales report, the cracks are beginning to show, and the currency is due for a correction. Retail sales rose only 0.1% in April, which is a dramatic slowdown from the 1.3% increase in the previous month. We’ve also been sceptical of how much longer we’ll see CAD data surprise to the upside, because at some point Canada will feel the sting of weaker global growth. And now that we’ve seen the first sign of weakness, there should be a stronger sell-off in the loonie.

EURO

Data review

- EZ trade balance 15.3bil vs 17bil expected

- EZ CPI 0.1% vs 0.2% expected

- EZ ZEW -20.2 vs -1.6 expected

- German ZEW current 7.8 vs 6.1 expected

- German ZEW expectations -21.1 vs -5.6 expected

- EZ PPI -0.1% vs 0.1% expected

- ECB current account 20.9bil vs 24.7bil previous

- GE PMI manufacturing 45.4 vs 44.6 expected

- GE PMI services 55.6 vs 55.2 expected

- GE PMI composite 52.6 vs 52.5 expected

- EZ PMI manufacturing 47.8 vs 48 expected

- EZ PMI services 53.4 vs 53 expected

- EZ PMI composite 52.1 vs 52 expected

Data preview

- German IFO: potential downside surprise given lower factory orders, industrial production and ZEW

- German CPI: potential downside surprise given lower oil prices in May and weaker PPI

- EZ confidence: confidence likely to be dampened by softer manufacturing activity

- EZ CPI: potential downside surprise given lower oil prices in May and weaker PPI

Key levels

- Support 1.1300

- Resistance 1.1500

Is euro rally sustainable?

The European Central Bank may be dovish, but the unexpected U-turn by the Federal Reserve drove EUR/USD to its highest level in two months. Stronger-than-expected eurozone PMI numbers also gave investors hope that the ECB could delay easing. In the forex market, currencies are driven by the latest turn of events. While the ECB talked rate cuts for the first time earlier this month, the most recent shift came from the Fed, and the market was positioned the wrong way. The euro was deeply oversold, and while some investors expected the Fed to be dovish, no one expected eight members to flip their views and start favouring a rate cut this year. As a result, EUR/USD shot higher breaking above all major moving averages, opening the door to a stronger move up to 1.1500. We don’t expect this week’s economic reports to help the currency, but the move in the euro right now is driven entirely by the market’s appetite for US dollar. It’s no secret that the EZ economy is slowing and inflation weakening, but should any of this week’s economic reports surprise to the upside, it’d give EUR/USD traders a stronger reason to bid up the currency.

BRITISH POUND

Data review

- Bank of England leaves rates unchanged and acknowledges global risks, but says if forecast holds, hike may be needed.

- CPI MoM 0.3% vs 0.3% expected

- CPI YoY 2% vs 2% expected

- CPI core 1.7% vs 1.6% expected

- PPI input 0% vs 0.2% expected

- PPI output 0.3% vs 0.2% expected

- Retail sales -0.5% vs -0.5% expected

- Retail sales ex autos -0.3% vs -0.4% expected

Data preview

- Q1 GDP revisions: Revisions are hard to predict, but changes will be market-moving.

Key levels

- Support 1.2600

- Resistance 1.2800

BoE still sees higher rates as next move

Like their peers, the Bank of England felt more cautious about global growth and raised concerns about greater downside risks. Yet, according to their monetary policy statement, they still believe that if their forecasts are correct, tighter monetary policy will be needed. This explains why, after falling initially, sterling recovered quickly. Until Britain decides how they want to finalise Brexit, the BoE will refrain from raising interest rates. But if global trade tensions continue to sour and world growth slows further, they may need to flip the switch and start talking about easing. The economy isn’t doing great, according to the latest economic reports. Retail sales fell for the second month in a row by -0.5%, which took the year-over-year rate down to 2.3% from 5.1%. There was no post-meeting press conference and, during his annual mansion speech, BoE Governor Mark Carney didn’t comment on monetary policy. While the Tory leadership contest holds the currency back, the BoE’s less dovish outlook could drive the pair well above 1.28.

The material provided here has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such is considered to be a marketing communication. Whilst it is not subject to any prohibition on dealing ahead of the dissemination of investment research we will not seek to take any advantage before providing it to our clients.

Pepperstone doesn’t represent that the material provided here is accurate, current or complete, and therefore shouldn’t be relied upon as such. The information, whether from a third party or not, isn’t to be considered as a recommendation; or an offer to buy or sell; or the solicitation of an offer to buy or sell any security, financial product or instrument; or to participate in any particular trading strategy. It does not take into account readers’ financial situation or investment objectives. We advise any readers of this content to seek their own advice. Without the approval of Pepperstone, reproduction or redistribution of this information isn’t permitted.